library(ggplot2)

library(MTS)

library(vars)Tema 2: Análisis multivariado de series temporales(2)

1 librerías

2 Ejemplo de VAR(2) simulado

set.seed(1000)

Phi_1 <- matrix(c(0.5, 0.1,

0.2, 0.4), nrow = 2, byrow = TRUE)

Phi_2 <- matrix(c(0.2, -0.1,

0.1, 0.3), nrow = 2, byrow = TRUE)

Sigma <- matrix(c(0.1, 0.02,

0.02, 0.1), nrow = 2)

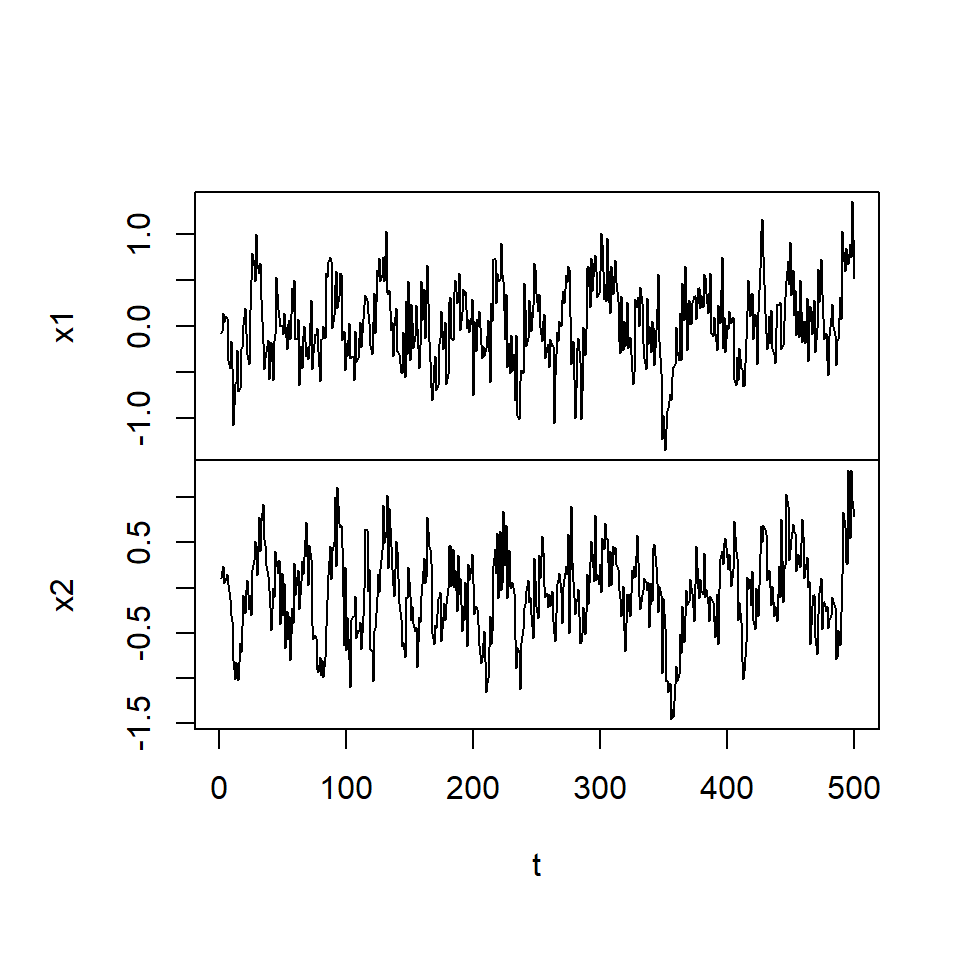

simVAR2 <- VARMAsim(nobs = 500, arlags = c(1, 2), phi = cbind(Phi_1, Phi_2), sigma = Sigma)

simVAR2_datos <- ts(simVAR2$series, names = c("x1", "x2"))

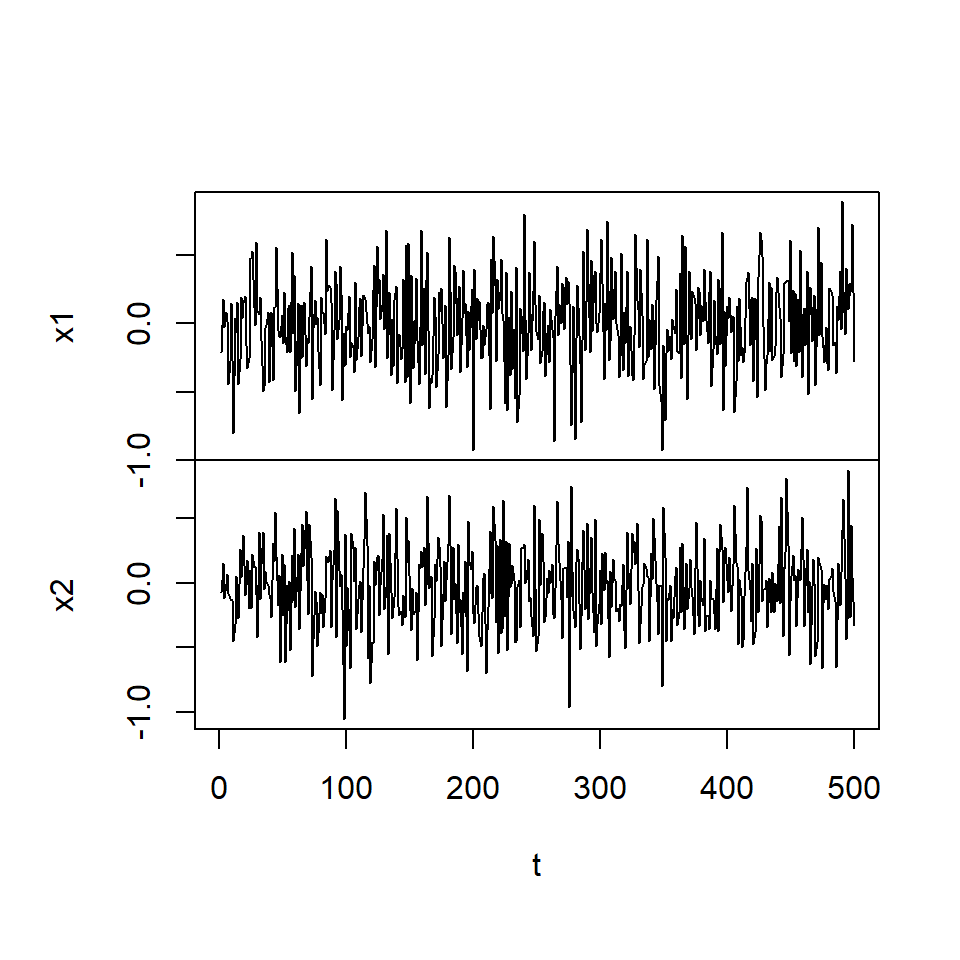

simVAR2_errores <- ts(simVAR2$noises, names = c("x1", "x2"))plot.ts(simVAR2_datos, main = "", xlab = "t")

plot.ts(simVAR2_errores, main = "", xlab = "t")

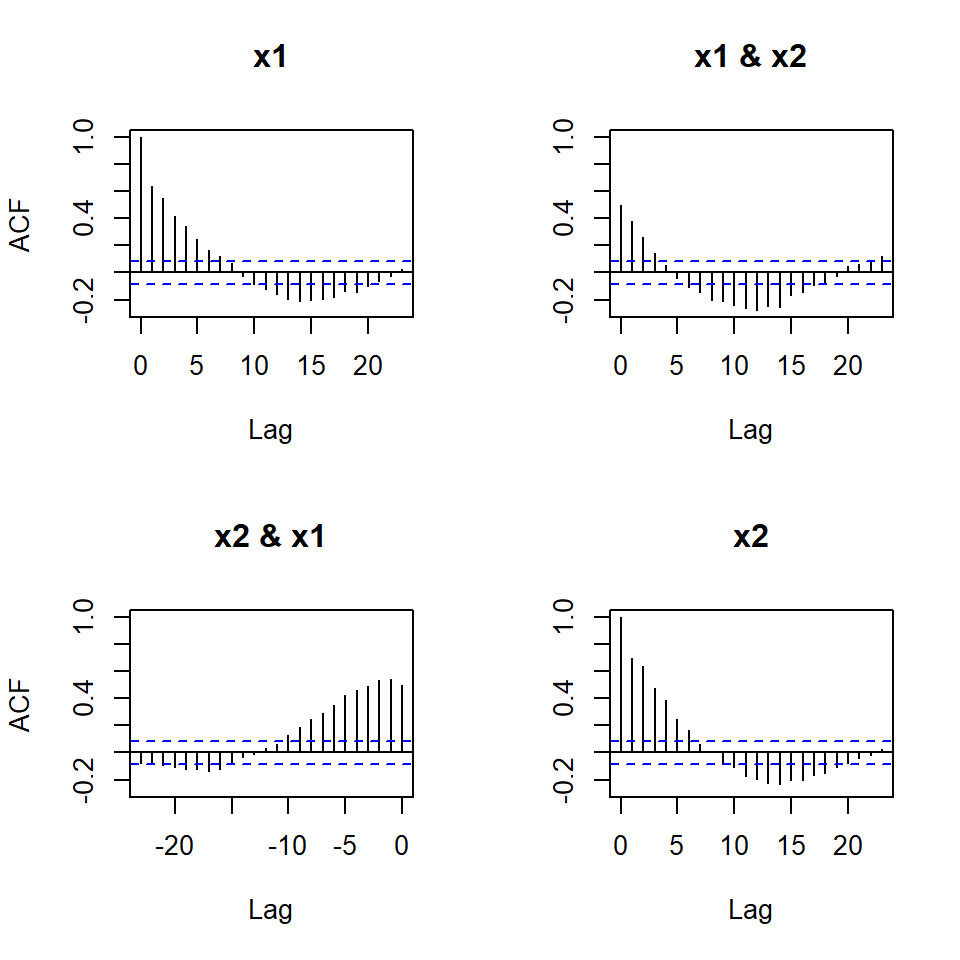

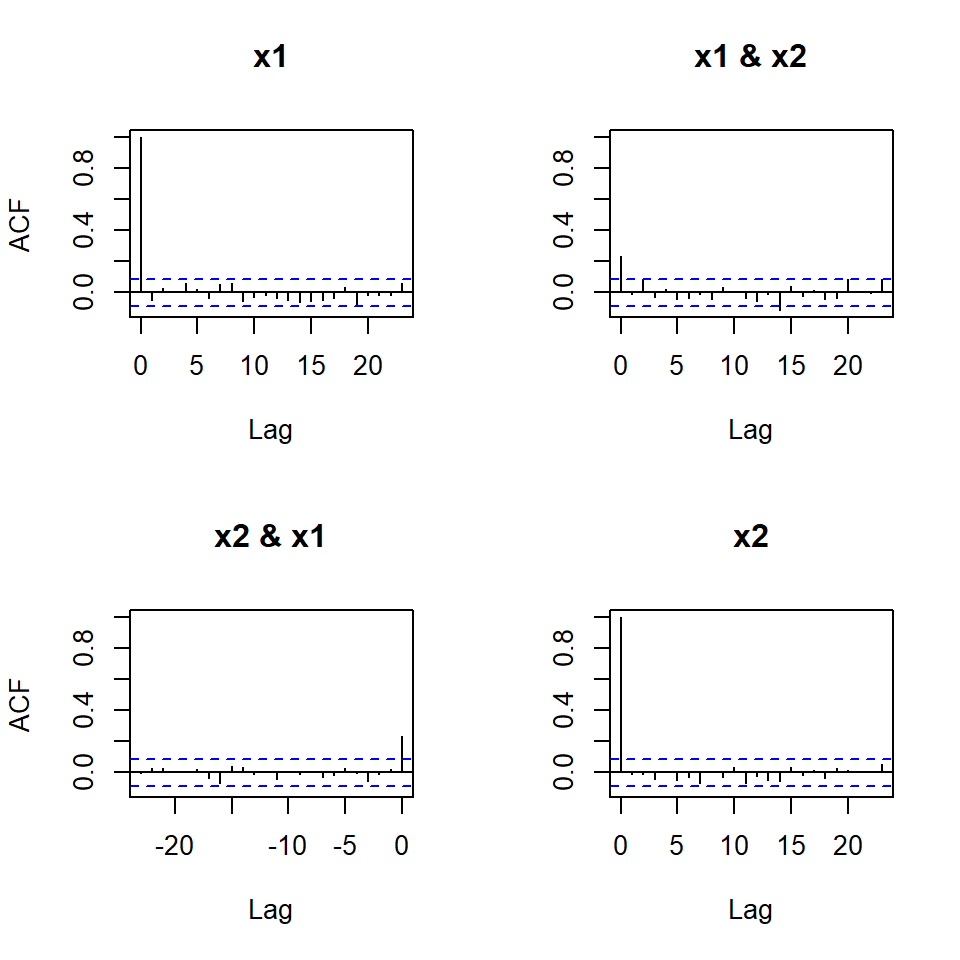

stats::acf(simVAR2_datos)

stats::acf(simVAR2_errores)

2.1 Determinar el lag de acuerdo a los criterios

infocrit <- vars::VARselect(simVAR2_datos, lag.max = 5,

type = "none")

infocrit$selection

AIC(n) HQ(n) SC(n) FPE(n)

2 2 2 2

$criteria

1 2 3 4 5

AIC(n) -4.49591313 -4.655845657 -4.654538769 -4.646930470 -4.640727992

HQ(n) -4.48257521 -4.629169805 -4.614524992 -4.593578768 -4.574038365

SC(n) -4.46193691 -4.587893208 -4.552610096 -4.511025573 -4.470846871

FPE(n) 0.01115449 0.009505878 0.009518325 0.009591051 0.0096507762.2 Estimar el modelo

varsimest <- vars::VAR(simVAR2_datos, p = 2, type = "none",

season = NULL, exogen = NULL)

summary(varsimest)

VAR Estimation Results:

=========================

Endogenous variables: x1, x2

Deterministic variables: none

Sample size: 498

Log Likelihood: -243.242

Roots of the characteristic polynomial:

0.7897 0.7897 0.3906 0.3329

Call:

vars::VAR(y = simVAR2_datos, p = 2, type = "none", exogen = NULL)

Estimation results for equation x1:

===================================

x1 = x1.l1 + x2.l1 + x1.l2 + x2.l2

Estimate Std. Error t value Pr(>|t|)

x1.l1 0.47772 0.04479 10.666 < 2e-16 ***

x2.l1 0.05368 0.04540 1.183 0.2375

x1.l2 0.26289 0.04725 5.564 4.34e-08 ***

x2.l2 -0.07826 0.04318 -1.812 0.0705 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3206 on 494 degrees of freedom

Multiple R-Squared: 0.4501, Adjusted R-squared: 0.4457

F-statistic: 101.1 on 4 and 494 DF, p-value: < 2.2e-16

Estimation results for equation x2:

===================================

x2 = x1.l1 + x2.l1 + x1.l2 + x2.l2

Estimate Std. Error t value Pr(>|t|)

x1.l1 0.22542 0.04312 5.228 2.54e-07 ***

x2.l1 0.37012 0.04370 8.469 2.86e-16 ***

x1.l2 0.07872 0.04549 1.730 0.0842 .

x2.l2 0.28505 0.04157 6.857 2.10e-11 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.3086 on 494 degrees of freedom

Multiple R-Squared: 0.5875, Adjusted R-squared: 0.5841

F-statistic: 175.9 on 4 and 494 DF, p-value: < 2.2e-16

Covariance matrix of residuals:

x1 x2

x1 0.10272 0.02334

x2 0.02334 0.09451

Correlation matrix of residuals:

x1 x2

x1 1.0000 0.2369

x2 0.2369 1.00002.3 Verificar que los eigenvalues tengan módulo menor a 1 (estacionariedad)

roots <- vars::roots(varsimest)

roots[1] 0.7897118 0.7897118 0.3906478 0.33287382.4 Diagnósticos

2.4.1 Prueba de Portmanteau

var2c.serial <- serial.test(varsimest, lags.pt = 16,

type = "PT.asymptotic")

var2c.serial

Portmanteau Test (asymptotic)

data: Residuals of VAR object varsimest

Chi-squared = 48.97, df = 56, p-value = 0.73582.4.2 Prueba de heteroscedasticidad

var2c.arch <- arch.test(varsimest, lags.multi = 5,

multivariate.only = TRUE)

var2c.arch

ARCH (multivariate)

data: Residuals of VAR object varsimest

Chi-squared = 70.045, df = 45, p-value = 0.0098162.4.3 Prueba de normalidad

var2c.norm <- normality.test(varsimest,

multivariate.only = TRUE)

var2c.norm$JB

JB-Test (multivariate)

data: Residuals of VAR object varsimest

Chi-squared = 1.3577, df = 4, p-value = 0.8515

$Skewness

Skewness only (multivariate)

data: Residuals of VAR object varsimest

Chi-squared = 0.90295, df = 2, p-value = 0.6367

$Kurtosis

Kurtosis only (multivariate)

data: Residuals of VAR object varsimest

Chi-squared = 0.45472, df = 2, p-value = 0.79662.4.4 Plot de los objetos “varcheck”

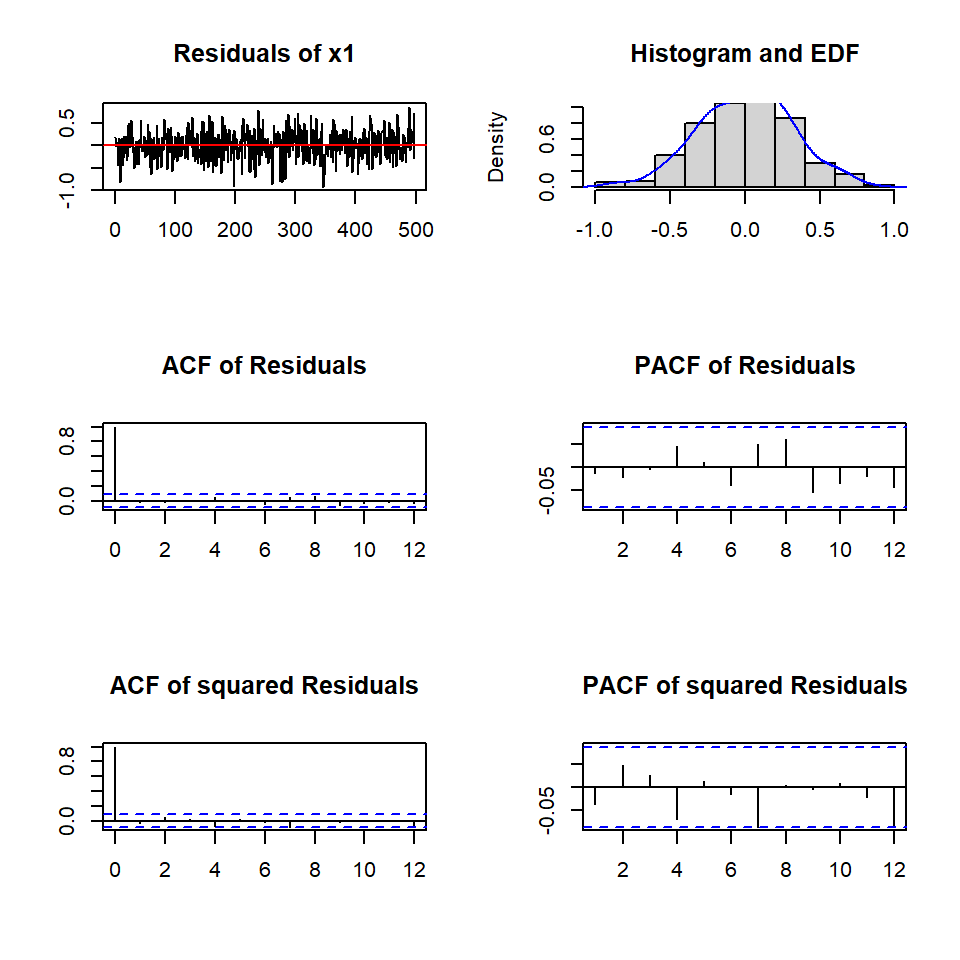

plot(var2c.serial, names = "x1")

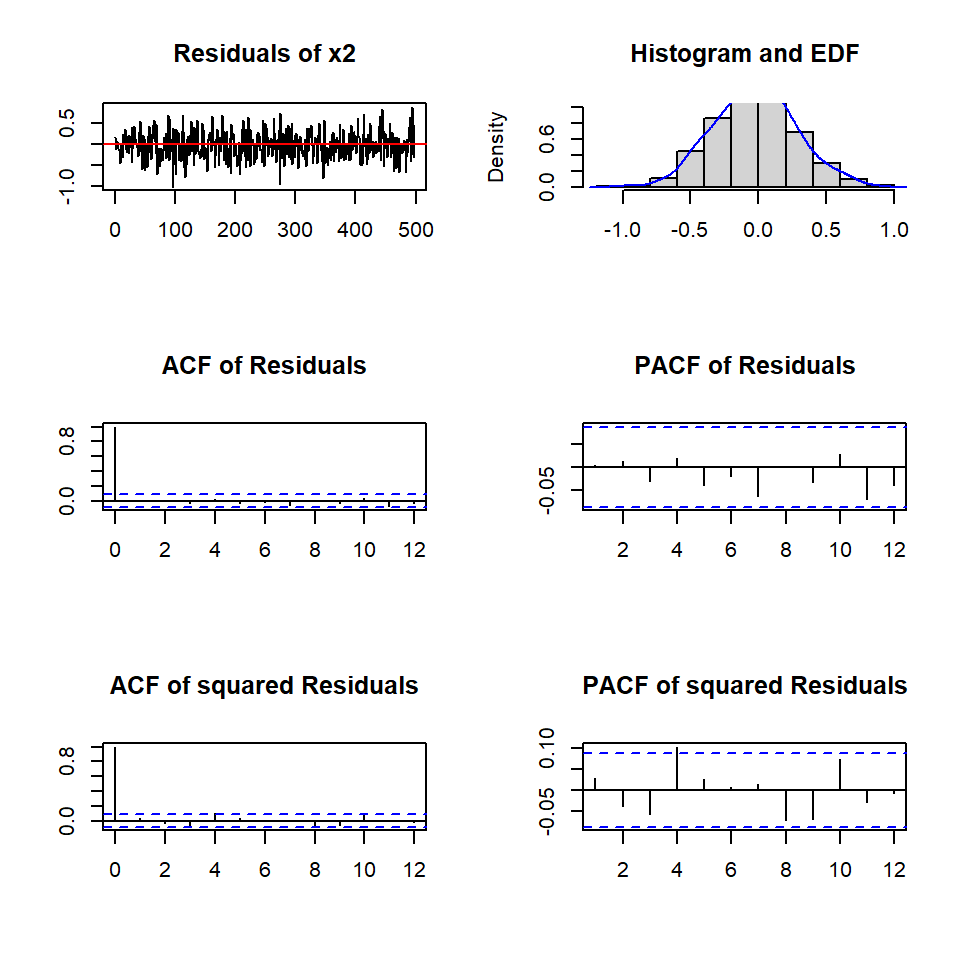

plot(var2c.serial, names = "x2")

2.5 Granger

var.causal.x1<- causality(varsimest,cause="x2")

var.causal.x1$Granger

Granger causality H0: x2 do not Granger-cause x1

data: VAR object varsimest

F-Test = 1.6496, df1 = 2, df2 = 988, p-value = 0.1927

$Instant

H0: No instantaneous causality between: x2 and x1

data: VAR object varsimest

Chi-squared = 25.836, df = 1, p-value = 3.716e-07var.causal.x2<- causality(varsimest,cause="x1")

var.causal.x2$Granger

Granger causality H0: x1 do not Granger-cause x2

data: VAR object varsimest

F-Test = 27.259, df1 = 2, df2 = 988, p-value = 2.996e-12

$Instant

H0: No instantaneous causality between: x1 and x2

data: VAR object varsimest

Chi-squared = 25.836, df = 1, p-value = 3.716e-072.6 Pronóstico

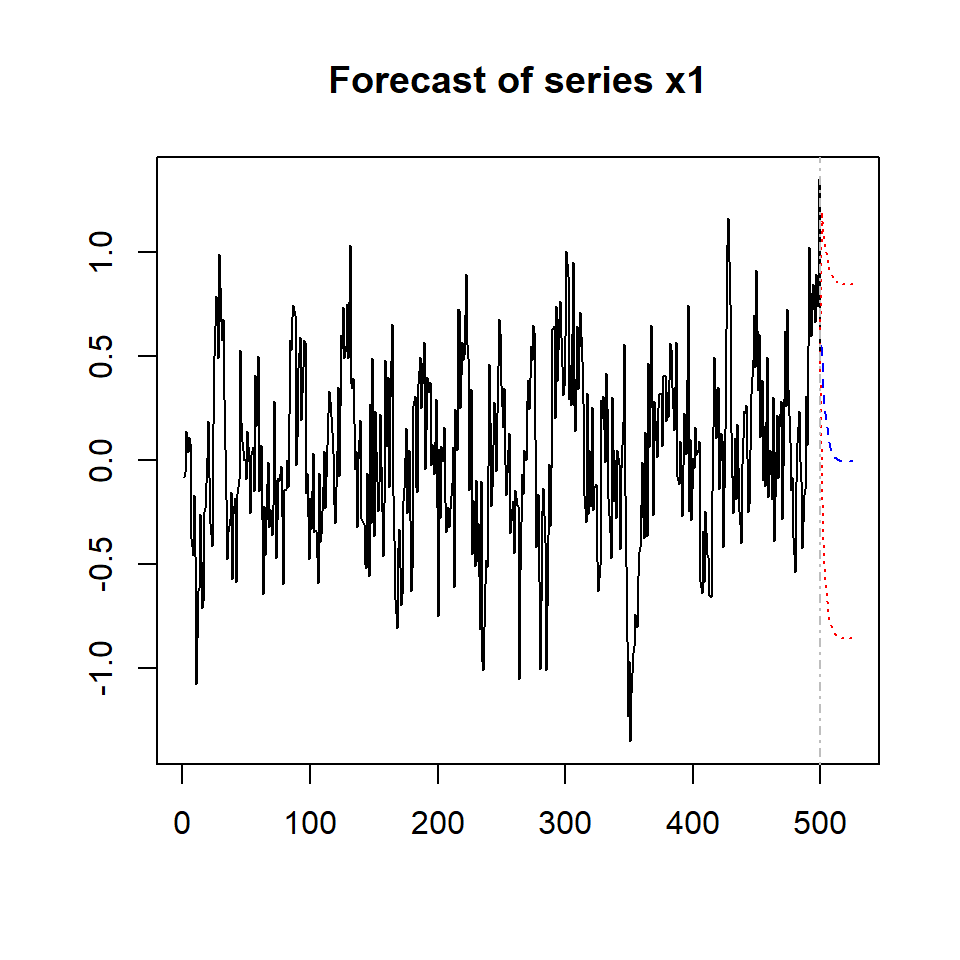

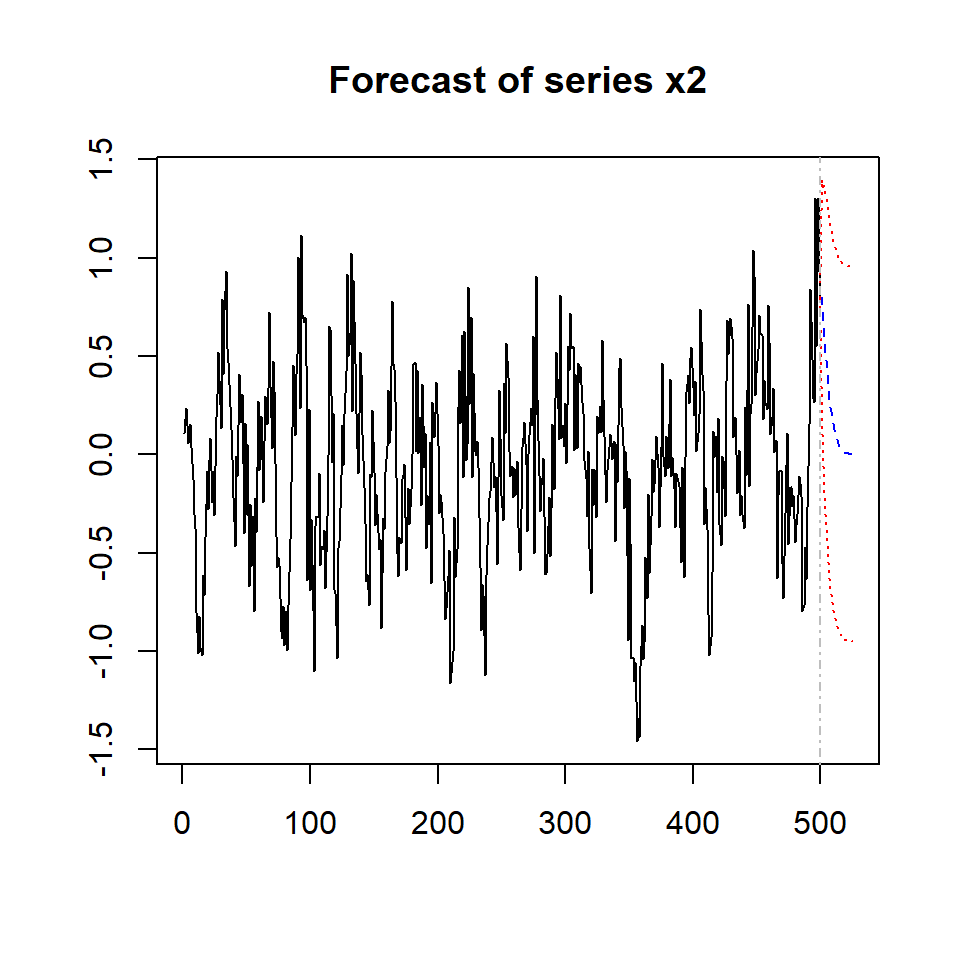

## Forecasting objects of class varest

predictions <- predict(varsimest, n.ahead = 25,

ci = 0.95)class(predictions)[1] "varprd"args(vars:::plot.varprd)function (x, plot.type = c("multiple", "single"), names = NULL,

main = NULL, col = NULL, lty = NULL, lwd = NULL, ylim = NULL,

ylab = NULL, xlab = NULL, nc, mar = par("mar"), oma = par("oma"),

...)

NULLplot(predictions, names = "x1")

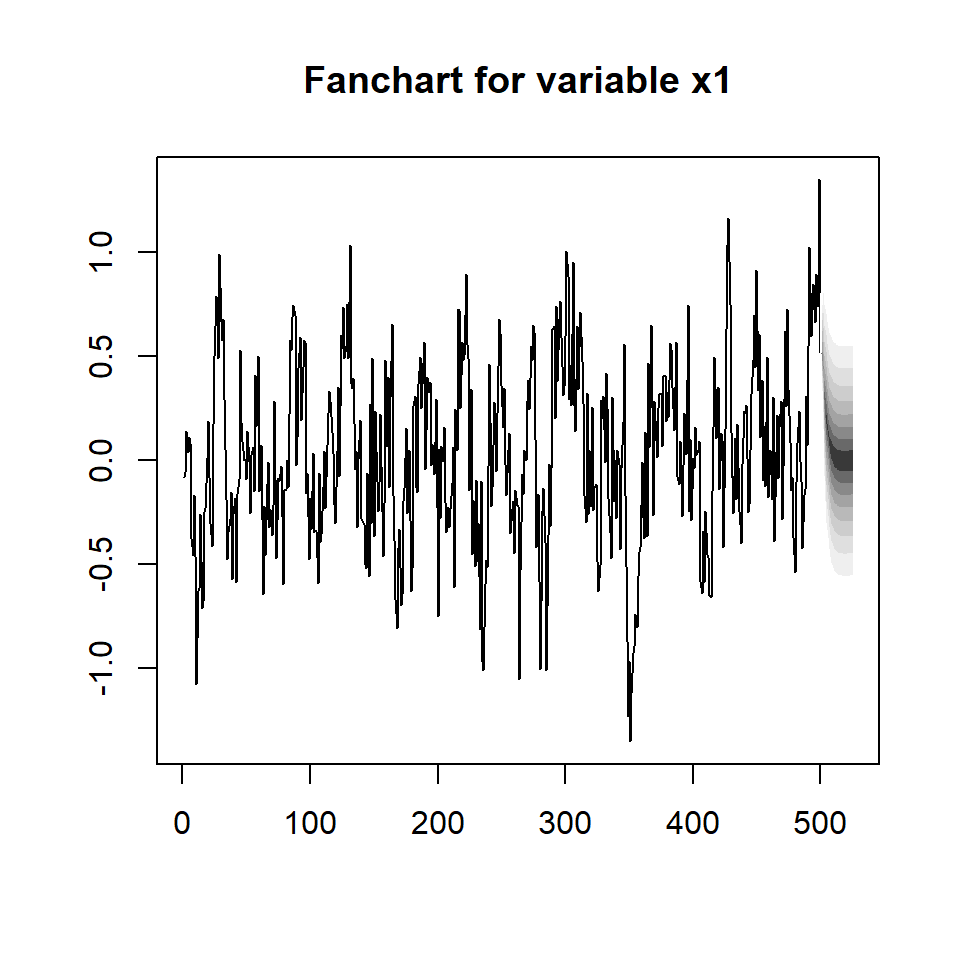

fanchart(predictions,names="x1")

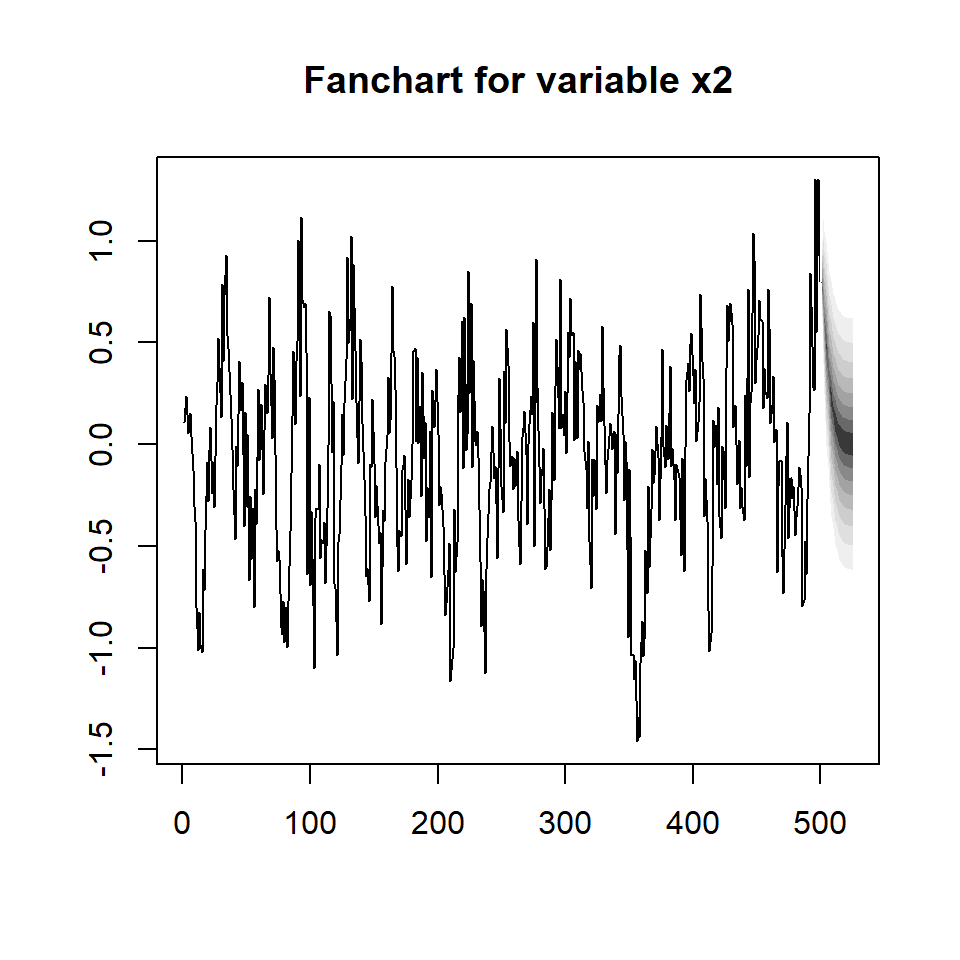

fanchart(predictions, names = "x2")

plot(predictions, names = "x2")

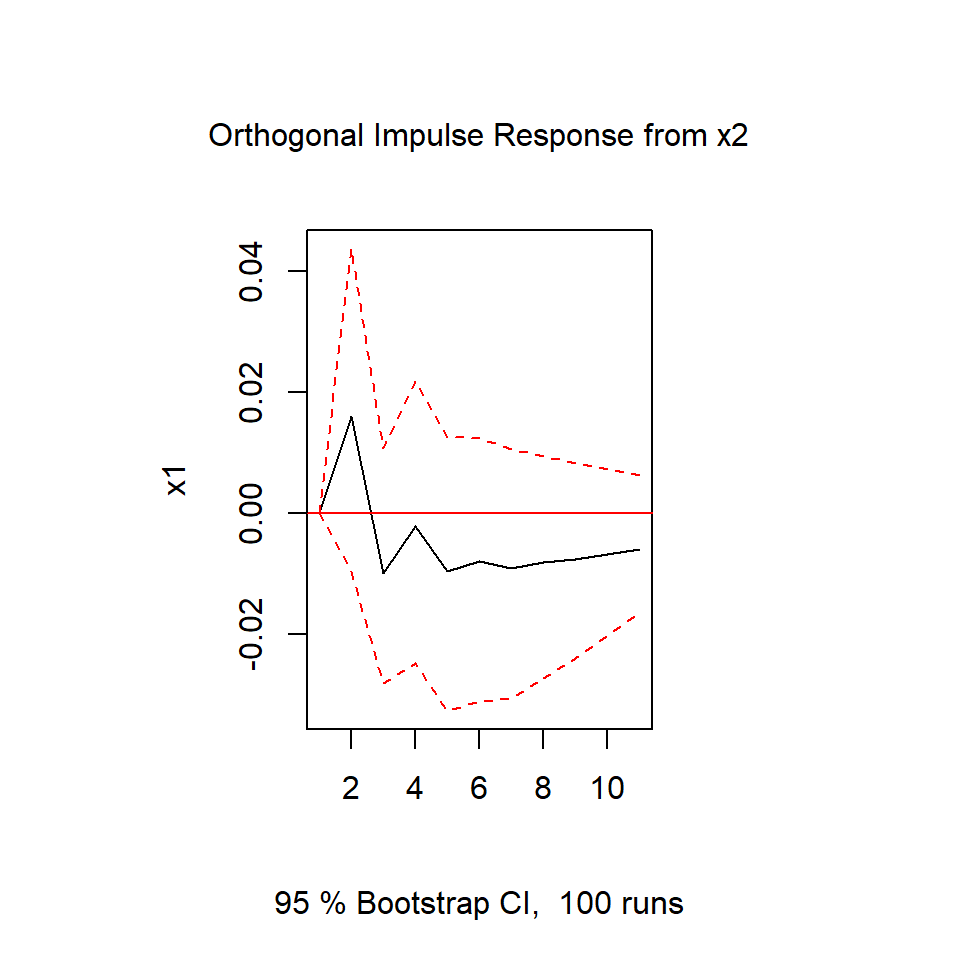

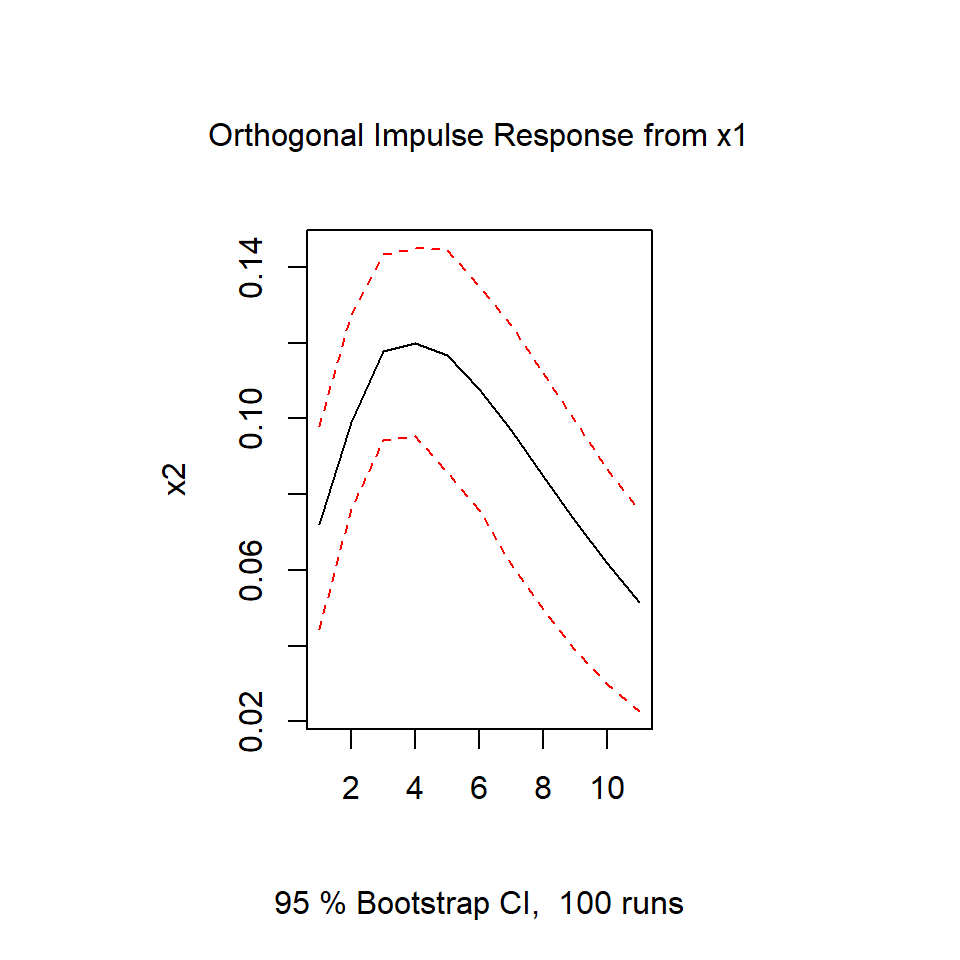

2.7 Función de impulso-respuesta

irf.x1 <- irf(varsimest, impulse = "x1",

response = "x2", n.ahead = 10)

plot(irf.x1)

irf.x2 <- irf(varsimest, impulse = "x2",

response = "x1", n.ahead = 10)

plot(irf.x2)