library(ggfortify)

library(forecast)

library(fpp2)

library(data.table)

library(TTR)

library(xts)

library(tidyverse)

library(lubridate)

library(DT)

library(quantmod)

library(plotly)Lab: Análisis exploratorio de series temporales

1 Librerías

2 Ejemplo: Pasajeros de avión

Totales mensuales de pasajeros de aerolíneas internacionales, de 1949 a 1960.

data("AirPassengers")

AirPassengers Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1949 112 118 132 129 121 135 148 148 136 119 104 118

1950 115 126 141 135 125 149 170 170 158 133 114 140

1951 145 150 178 163 172 178 199 199 184 162 146 166

1952 171 180 193 181 183 218 230 242 209 191 172 194

1953 196 196 236 235 229 243 264 272 237 211 180 201

1954 204 188 235 227 234 264 302 293 259 229 203 229

1955 242 233 267 269 270 315 364 347 312 274 237 278

1956 284 277 317 313 318 374 413 405 355 306 271 306

1957 315 301 356 348 355 422 465 467 404 347 305 336

1958 340 318 362 348 363 435 491 505 404 359 310 337

1959 360 342 406 396 420 472 548 559 463 407 362 405

1960 417 391 419 461 472 535 622 606 508 461 390 432Este objeto ya está definido con la clase ts.

class(AirPassengers)[1] "ts"Vamos a convertirlo como un vector numérico.

AP <- as.numeric(AirPassengers)

class(AP)[1] "numeric"Una serie temporal es, simplemente, un vector de observaciones indexado en el tiempo.

AP.data <- data.frame(tiempo=seq_along(AP),pasajero=AP)

head(AP.data) tiempo pasajero

1 1 112

2 2 118

3 3 132

4 4 129

5 5 121

6 6 135tail(AP.data) tiempo pasajero

139 139 622

140 140 606

141 141 508

142 142 461

143 143 390

144 144 4322.1 Gráficos de los valores de la serie contra el tiempo.

- Un gráfico de dispersión no es apropiado, pues no permite ilustar la secuencia natural de los datos.

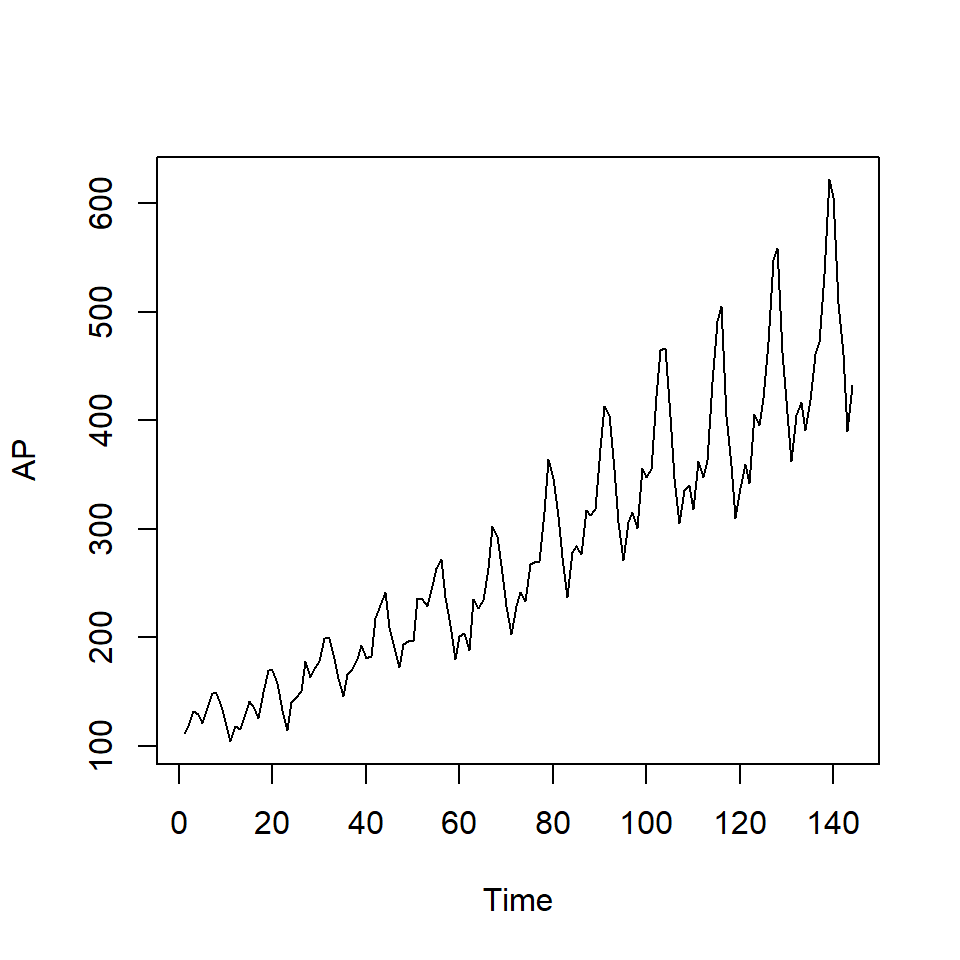

plot(AP.data$tiempo,AP.data$pasajero)

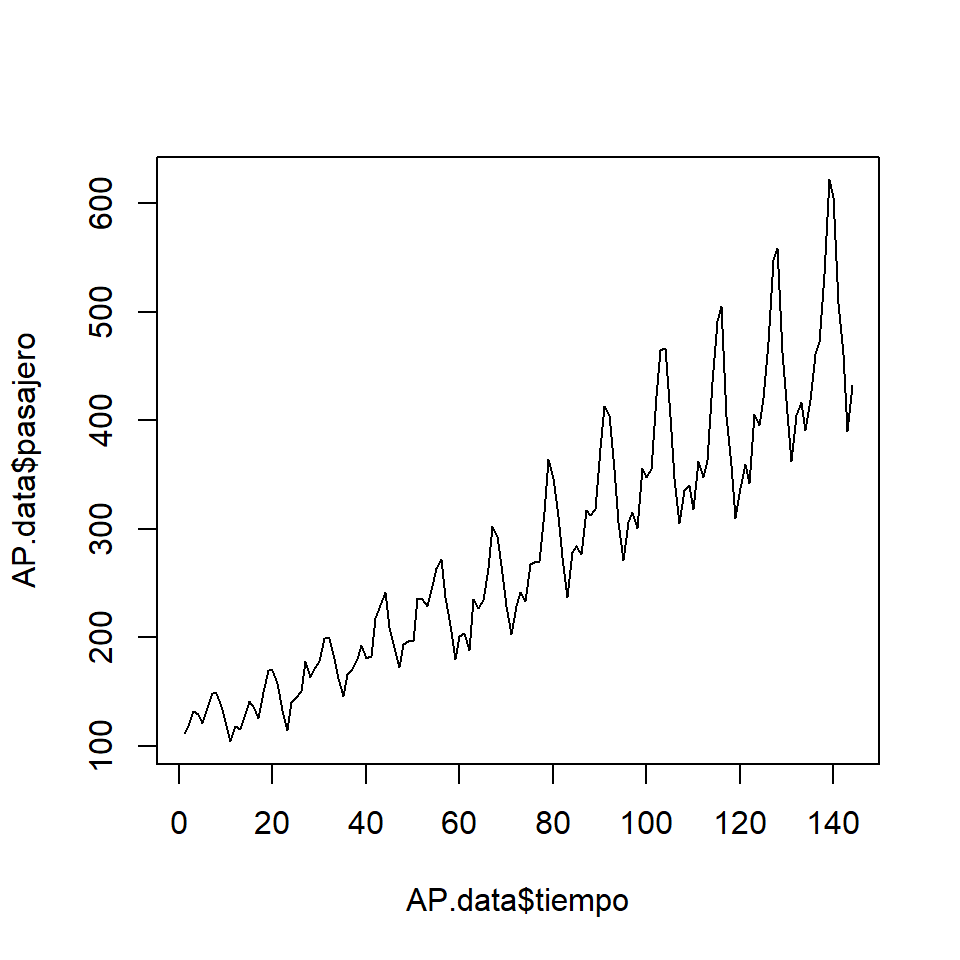

- Una forma es usar el argumento

type="l", otype="b".

plot(AP.data$tiempo,AP.data$pasajero,type="l")

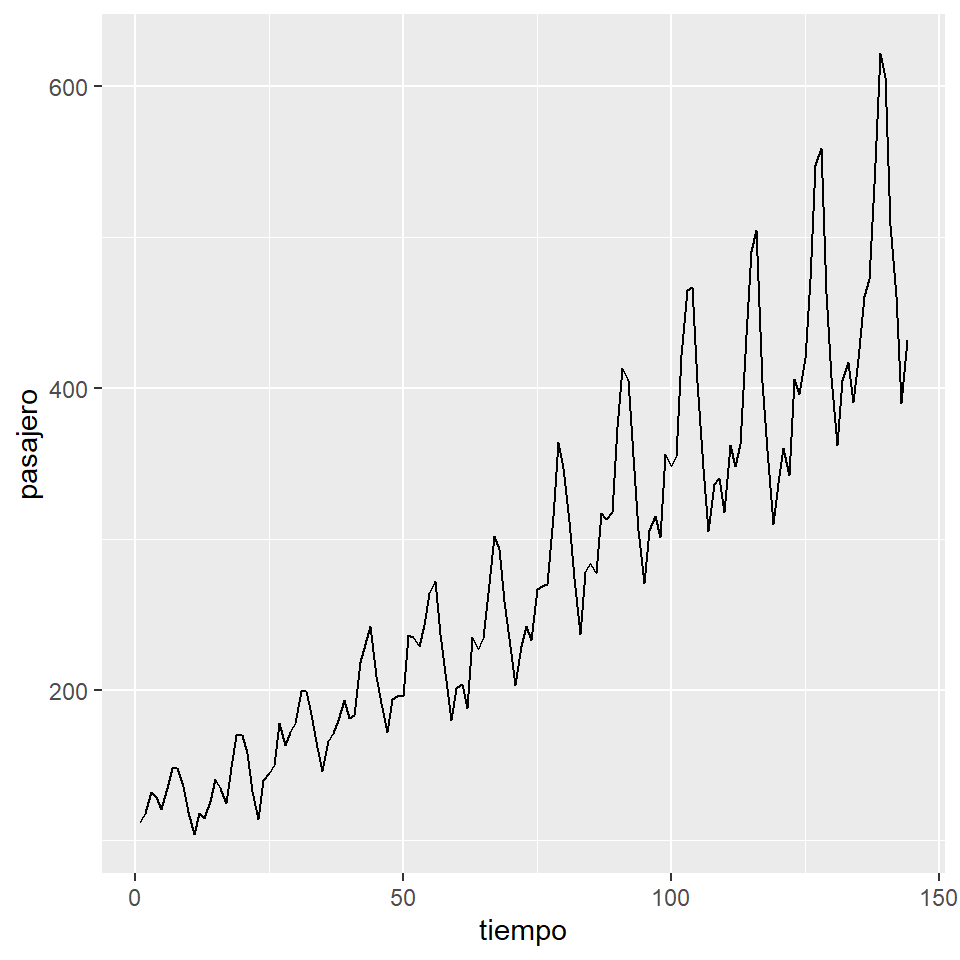

ggplot(AP.data, aes(x=tiempo,y=pasajero)) + geom_line()

- Diferentes objetos en R.

str(AirPassengers) Time-Series [1:144] from 1949 to 1961: 112 118 132 129 121 135 148 148 136 119 ...str(AP) num [1:144] 112 118 132 129 121 135 148 148 136 119 ...- Se define como un objeto

ts.

AP.ts <- ts(AP, start = c(1949, 1), frequency = 12)

str(AP.ts) Time-Series [1:144] from 1949 to 1961: 112 118 132 129 121 135 148 148 136 119 ...frequency(AP.ts) #la frecuencia de la serie[1] 12cycle(AP.ts) #verificar el ciclo de cada observación Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1949 1 2 3 4 5 6 7 8 9 10 11 12

1950 1 2 3 4 5 6 7 8 9 10 11 12

1951 1 2 3 4 5 6 7 8 9 10 11 12

1952 1 2 3 4 5 6 7 8 9 10 11 12

1953 1 2 3 4 5 6 7 8 9 10 11 12

1954 1 2 3 4 5 6 7 8 9 10 11 12

1955 1 2 3 4 5 6 7 8 9 10 11 12

1956 1 2 3 4 5 6 7 8 9 10 11 12

1957 1 2 3 4 5 6 7 8 9 10 11 12

1958 1 2 3 4 5 6 7 8 9 10 11 12

1959 1 2 3 4 5 6 7 8 9 10 11 12

1960 1 2 3 4 5 6 7 8 9 10 11 12- La función

plottoma en cuenta el tipo de objeto.

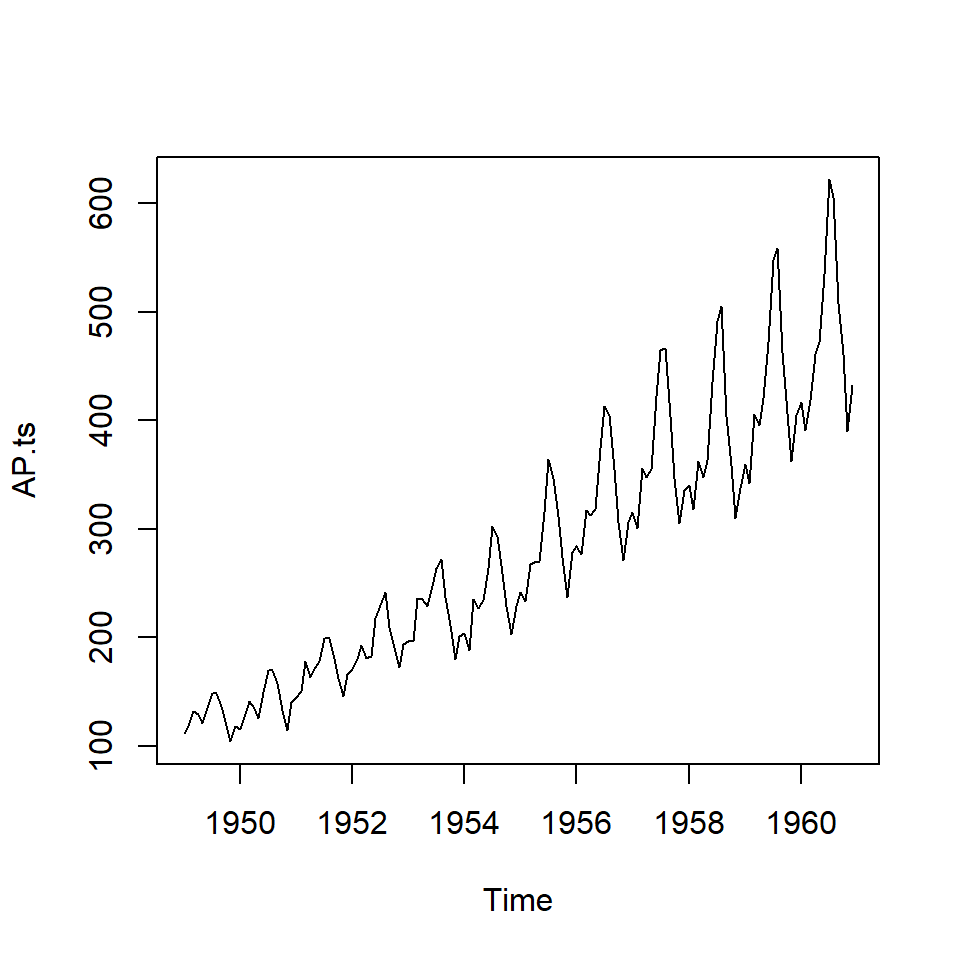

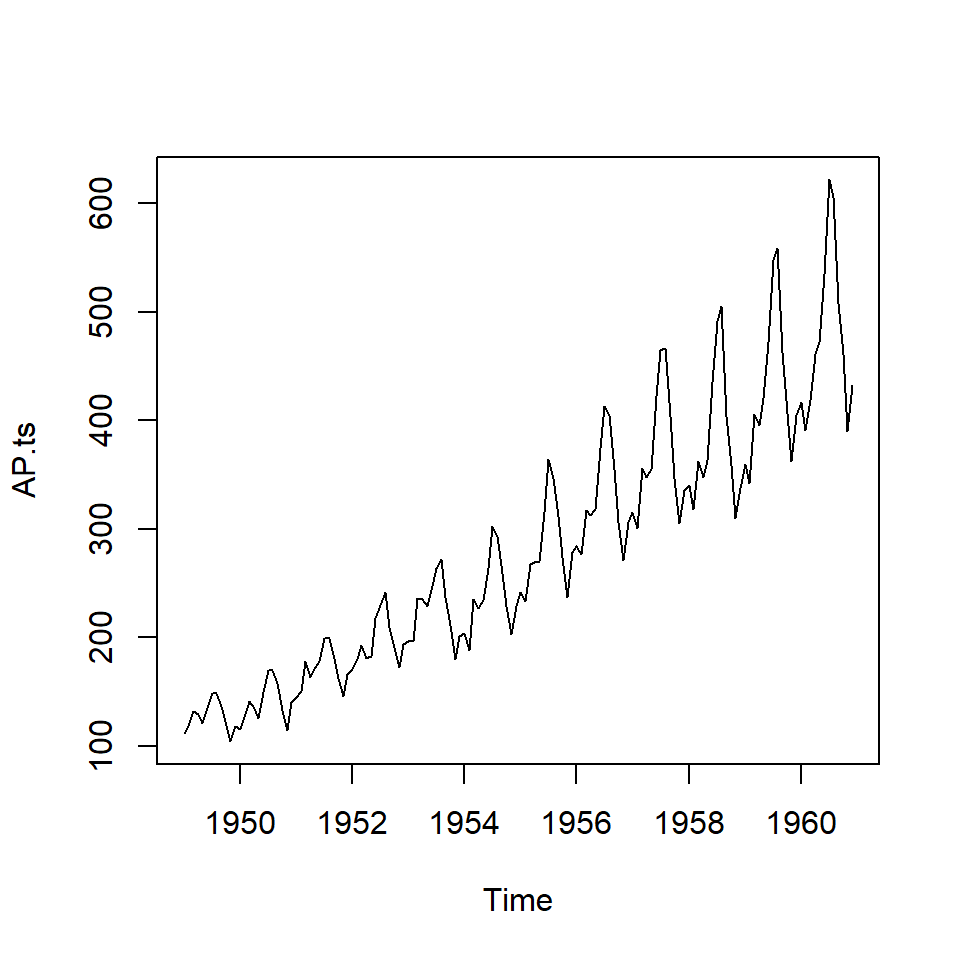

plot(AP)

plot(AP.ts)

- Se el objeto es

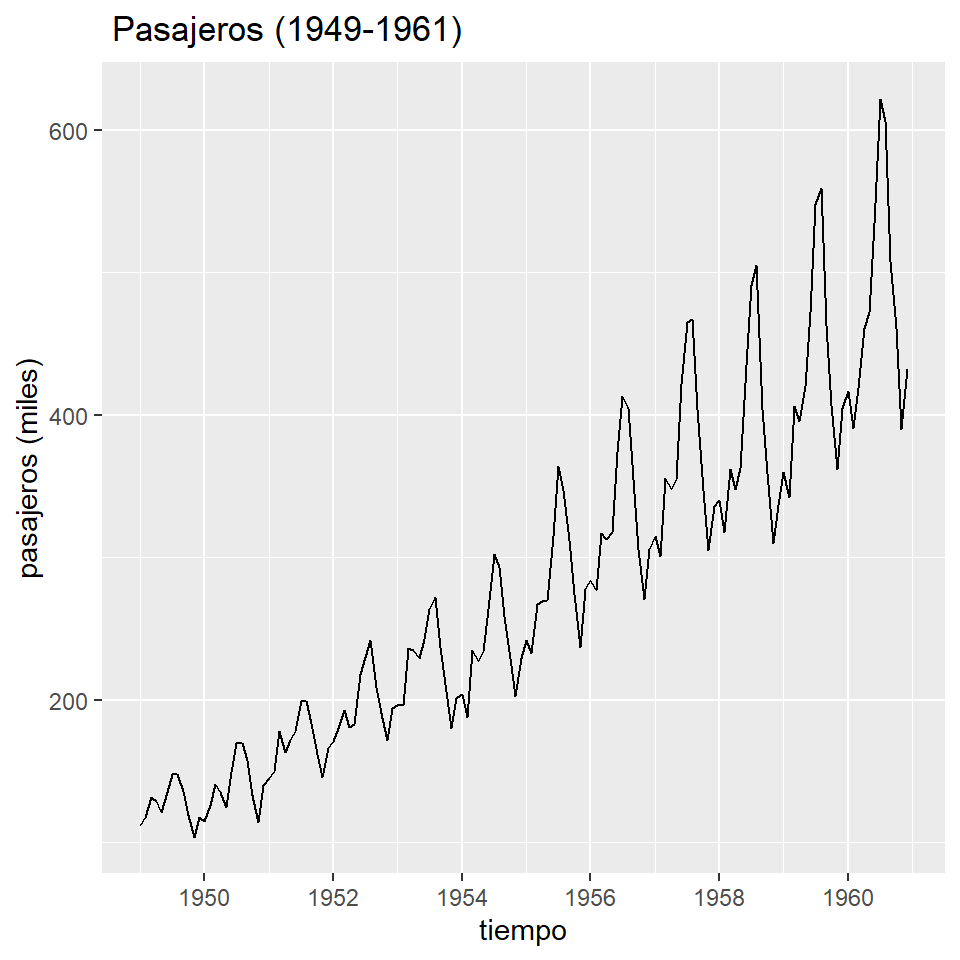

ts, la funciónautoplotlo detecta.

forecast::autoplot(AP.ts) + labs(x ="tiempo", y = "pasajeros (miles)", title=" Pasajeros (1949-1961)")

ts.plot(AP.ts) # Asume una serie temporal.

ts.plot(AP) # También asume una serie temporal aunque el objeto no es ts.

2.2 Otras opciones más personalizadas

- Personalizar el gráfico usando el vector de tiempo.

year <- rep(1949:1960,each=12)

month <- rep(1:12, times=12)

AP.data <- AP.data %>% mutate('year'=year, 'month'=month)

AP.data1 <- AP.data %>%

mutate(date = make_datetime(year = year, month = month))

AP.data1$date <- as.Date(AP.data1$date)

str(AP.data1)'data.frame': 144 obs. of 5 variables:

$ tiempo : int 1 2 3 4 5 6 7 8 9 10 ...

$ pasajero: num 112 118 132 129 121 135 148 148 136 119 ...

$ year : int 1949 1949 1949 1949 1949 1949 1949 1949 1949 1949 ...

$ month : int 1 2 3 4 5 6 7 8 9 10 ...

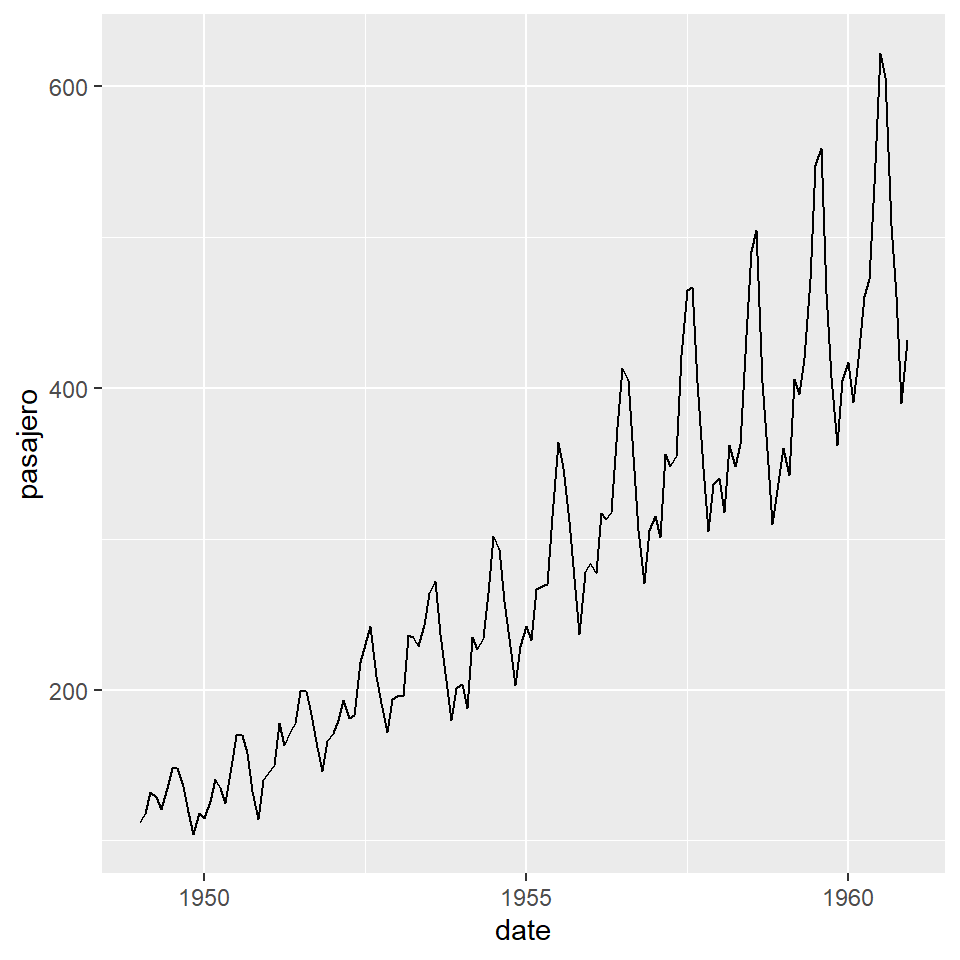

$ date : Date, format: "1949-01-01" "1949-02-01" ...plot1 <- ggplot(AP.data1, aes(x=date,y=pasajero)) +

geom_line()

plot1

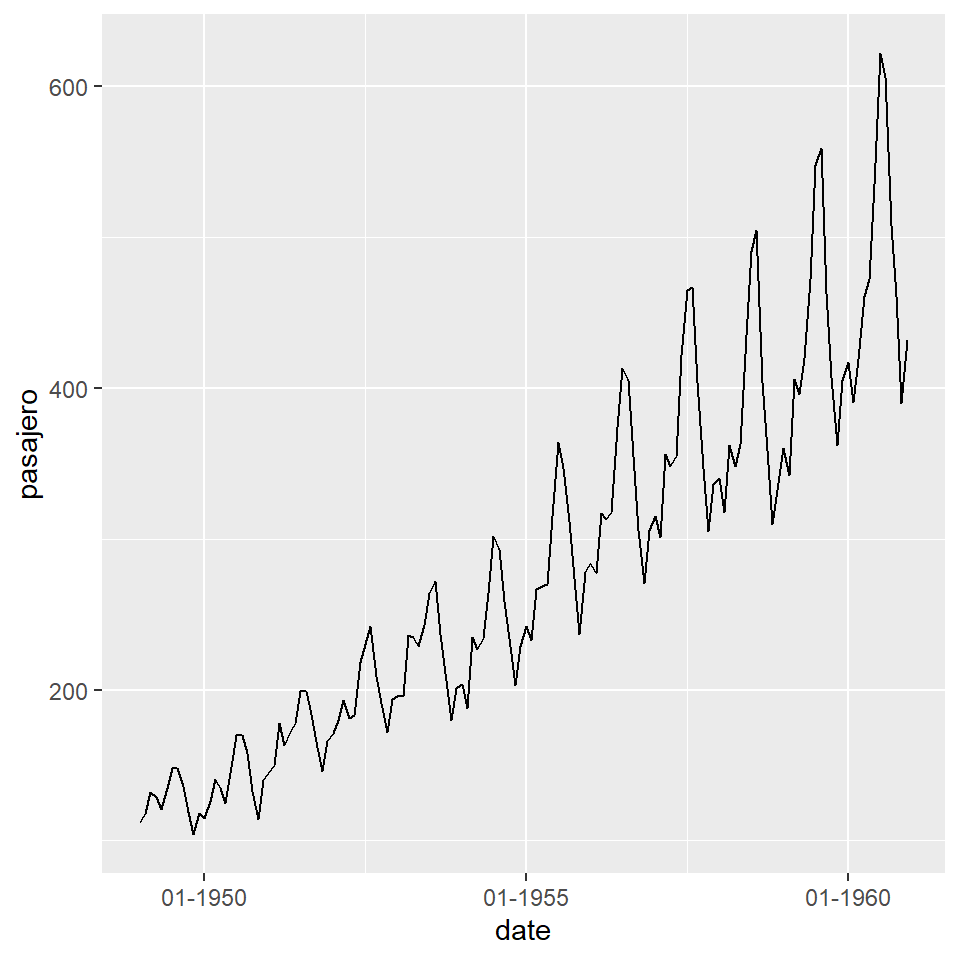

plot1 + scale_x_date(date_labels = "%m-%Y")

plot1 + scale_x_date(date_breaks = "1 month")

plot1 + scale_x_date(date_breaks = "6 month")

plot1 + scale_x_date(date_breaks = "1 year")

plot1 + scale_x_date(date_breaks = "2 year")

plot_ly(x = time(AirPassengers), y = as.numeric(AirPassengers), type = 'scatter', mode = 'lines') %>%

layout(title = "AirPassengers Time Series",

xaxis = list(title = "Time"),

yaxis = list(title = "Passengers"))2.3 Descomposición de series

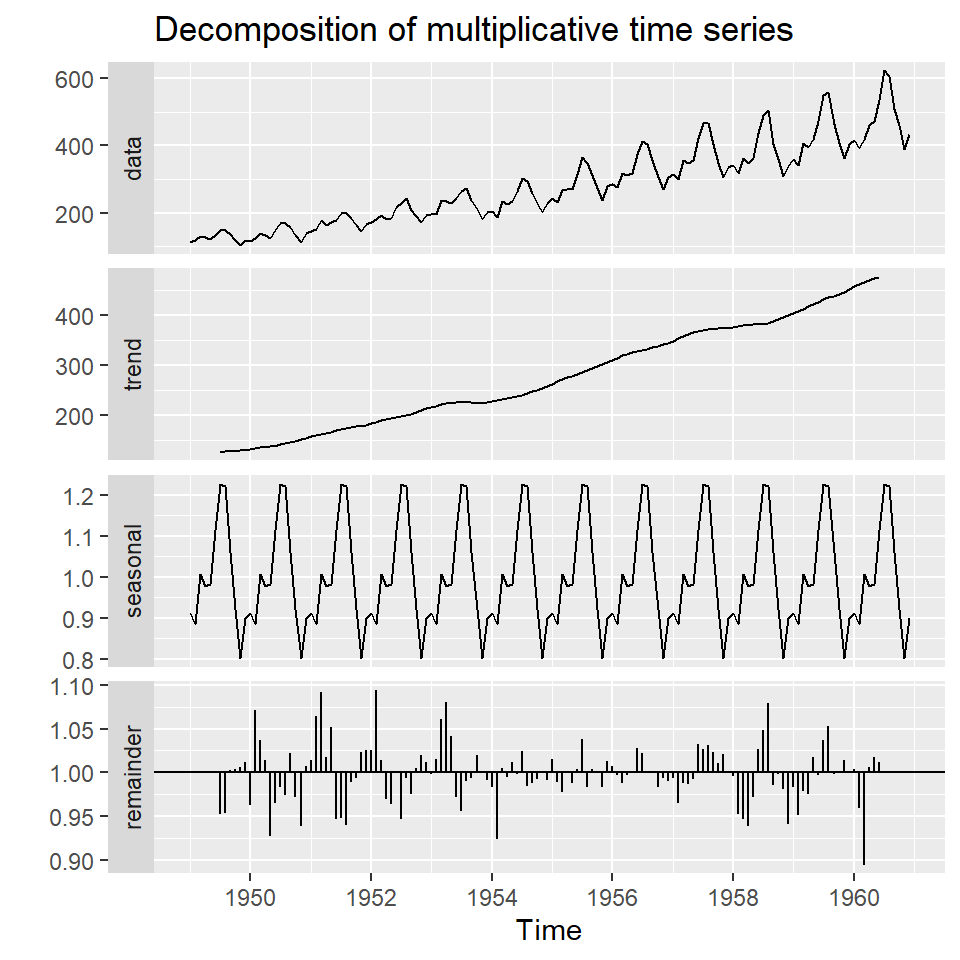

Más adelante veremos paso a paso la descomposición de series temporales.

decomposeAP <- decompose(AP.ts,"multiplicative")

autoplot(decomposeAP)

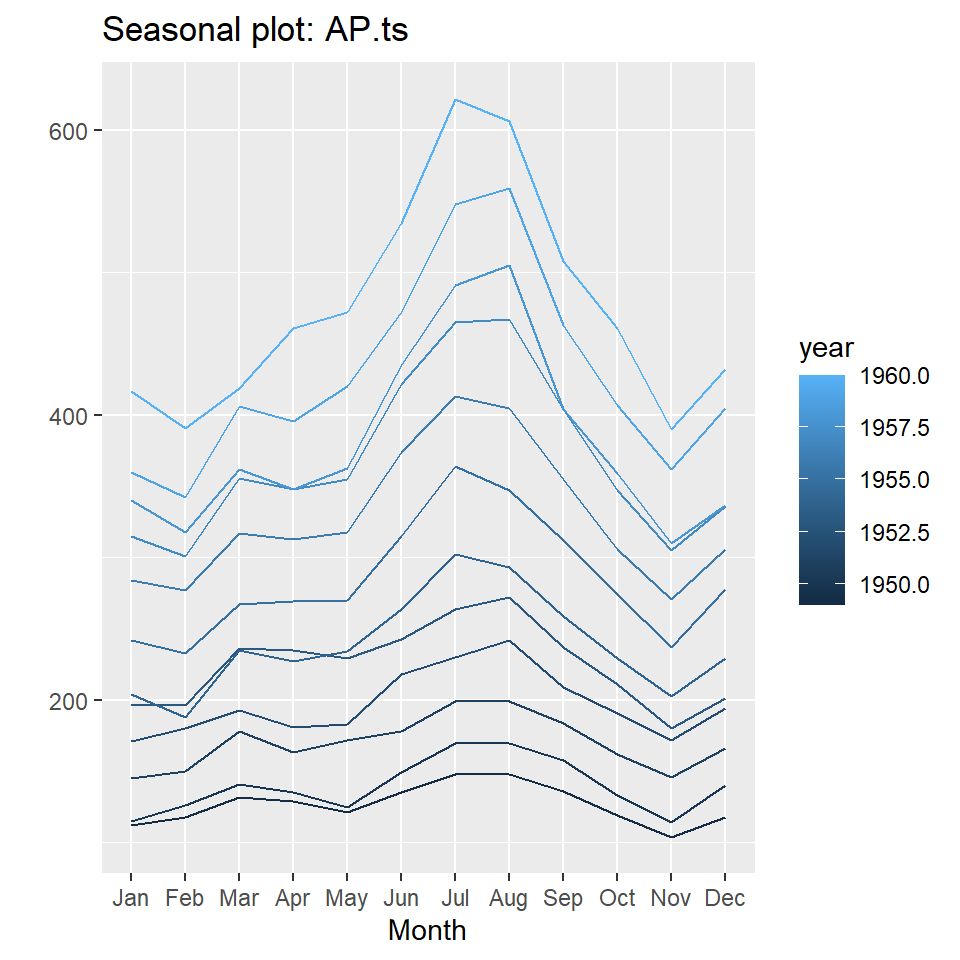

¿Qué notamos en este gráfico? tendencia, ciclos, estacionalidad.

2.4 Otros gráficos útiles para estudiar el efecto estacional

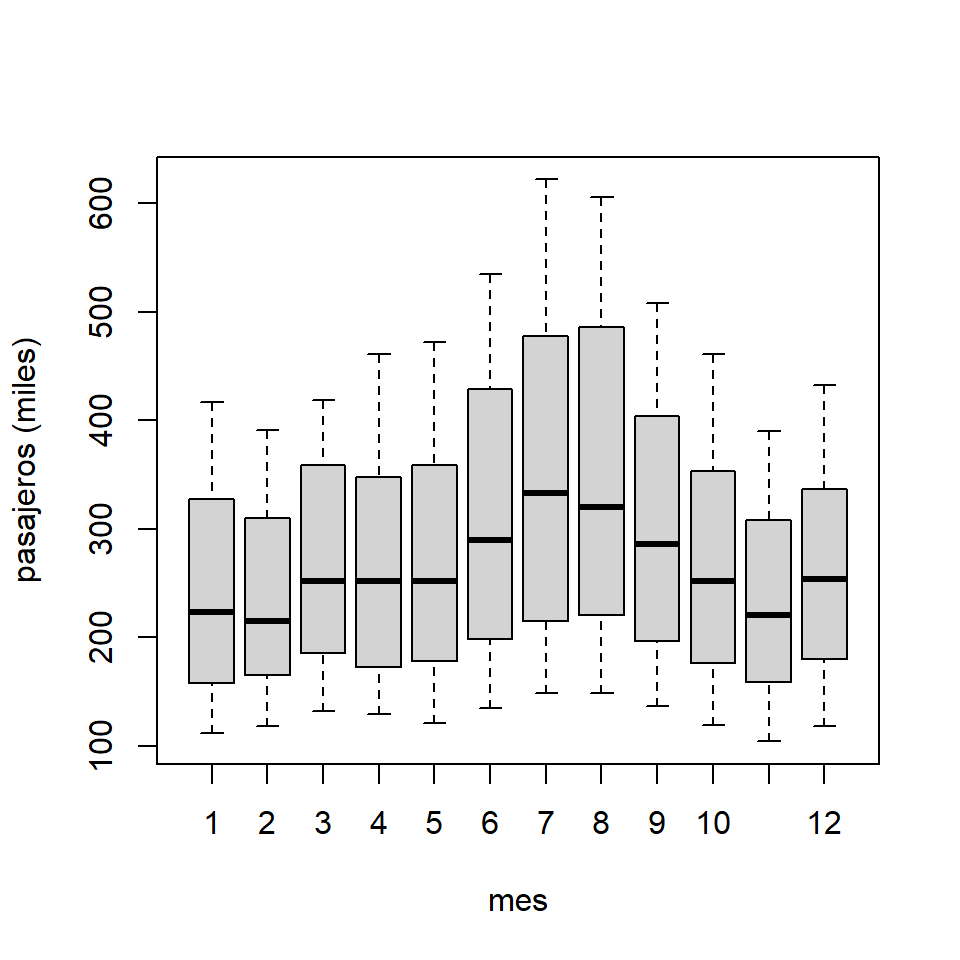

- El gráfico de caja no es útil pues no muestra la secuencia temporal.

boxplot(AP.ts~cycle(AP.ts),xlab="mes", ylab = "pasajeros (miles)")

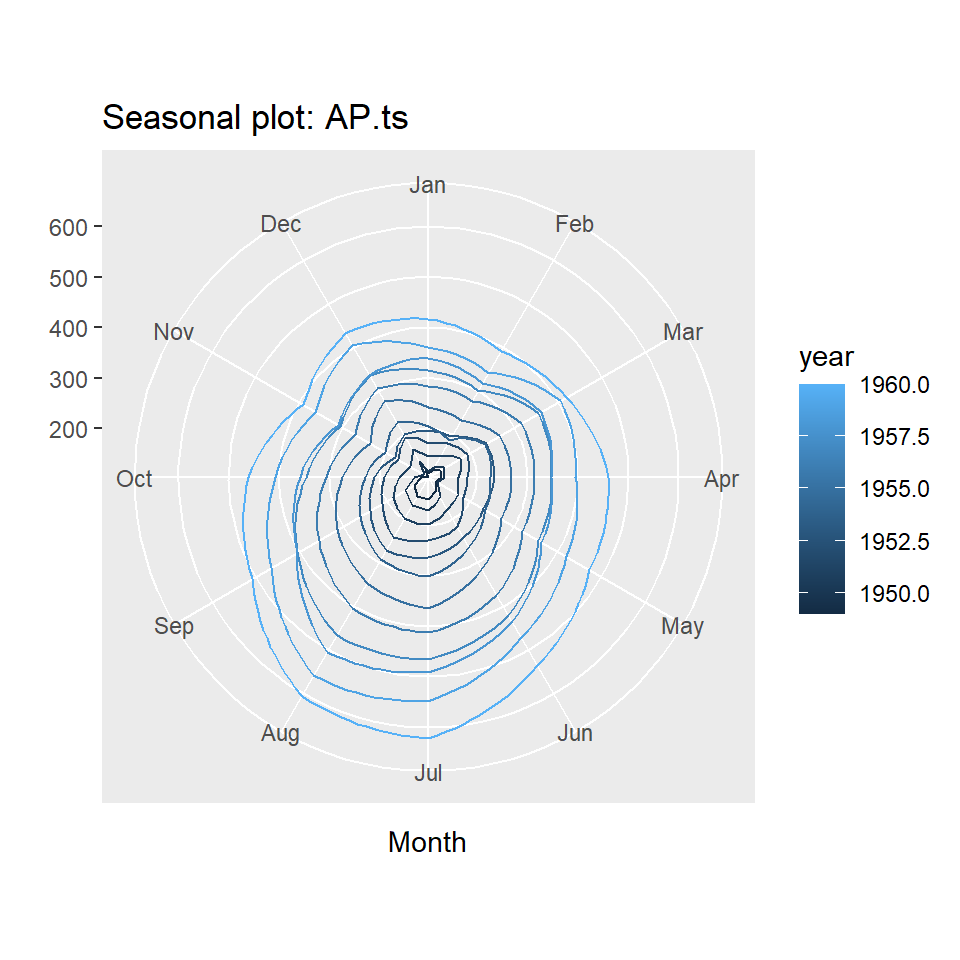

- Son más útiles los gráficos estacionales.

ggseasonplot(AP.ts, year.labels=FALSE, continuous=TRUE)

ggseasonplot(AP.ts, year.labels=FALSE, continuous=TRUE, polar = TRUE)

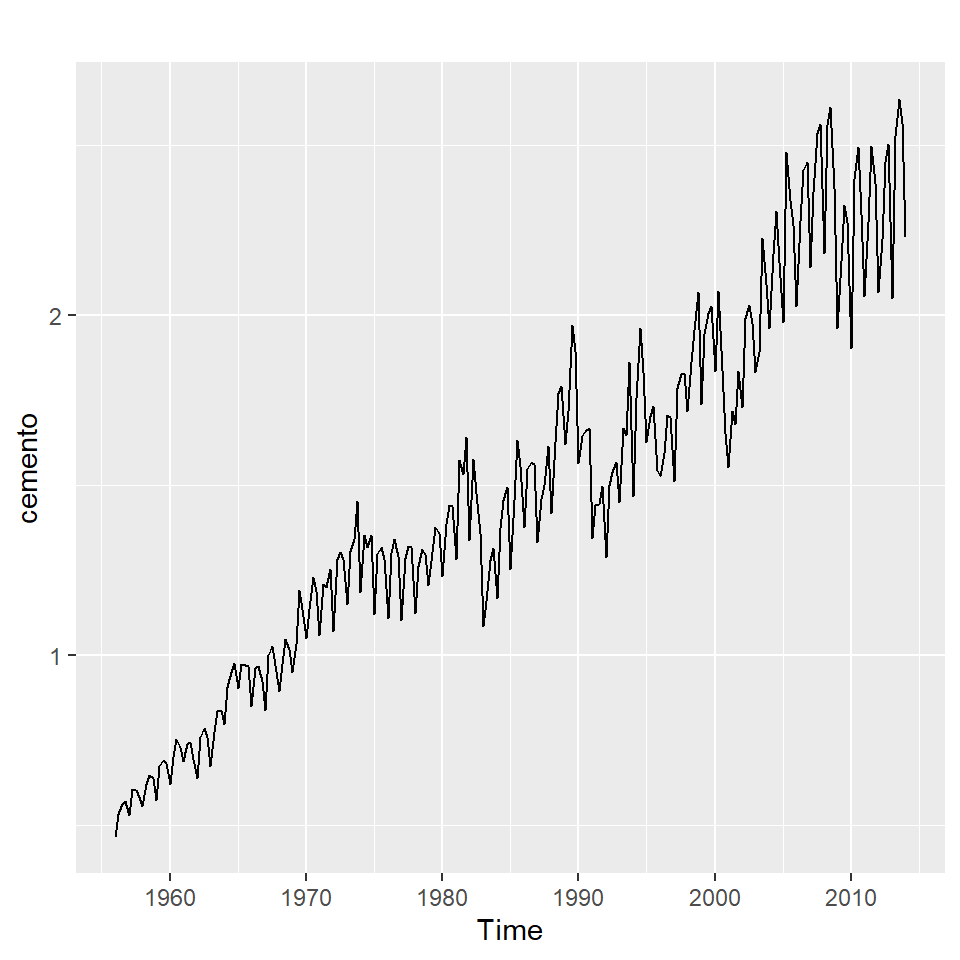

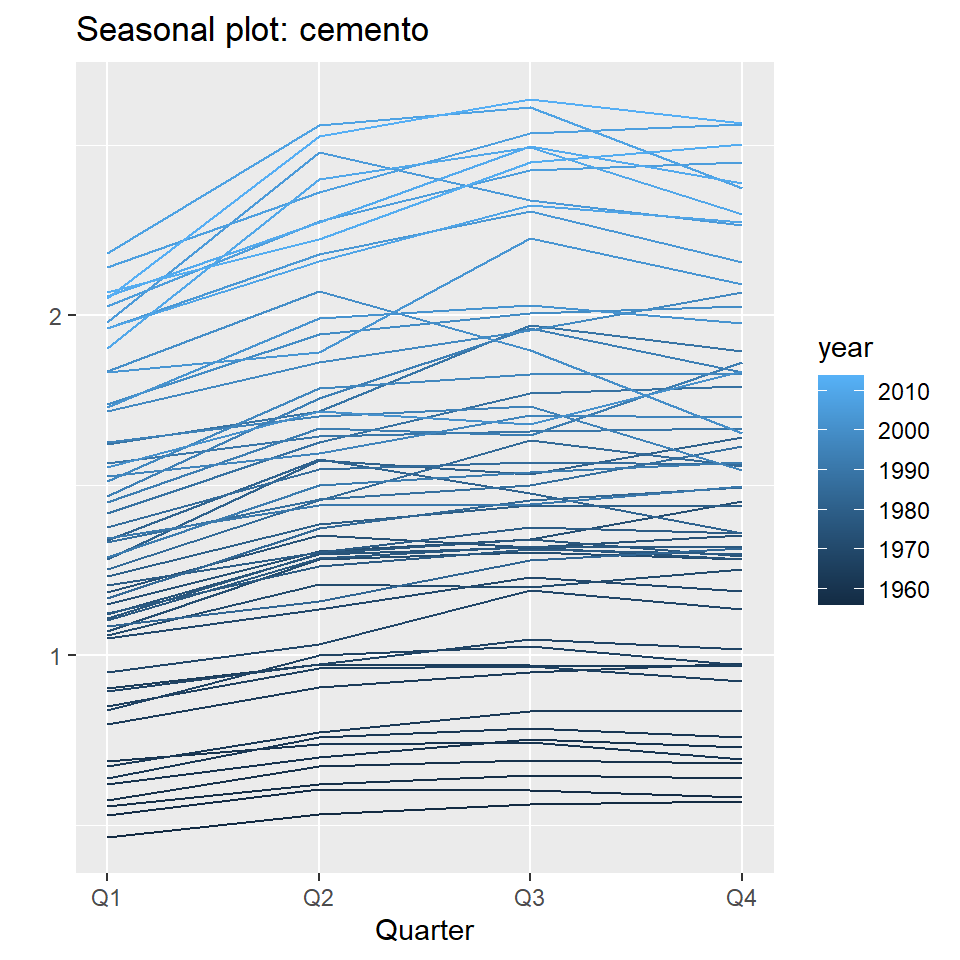

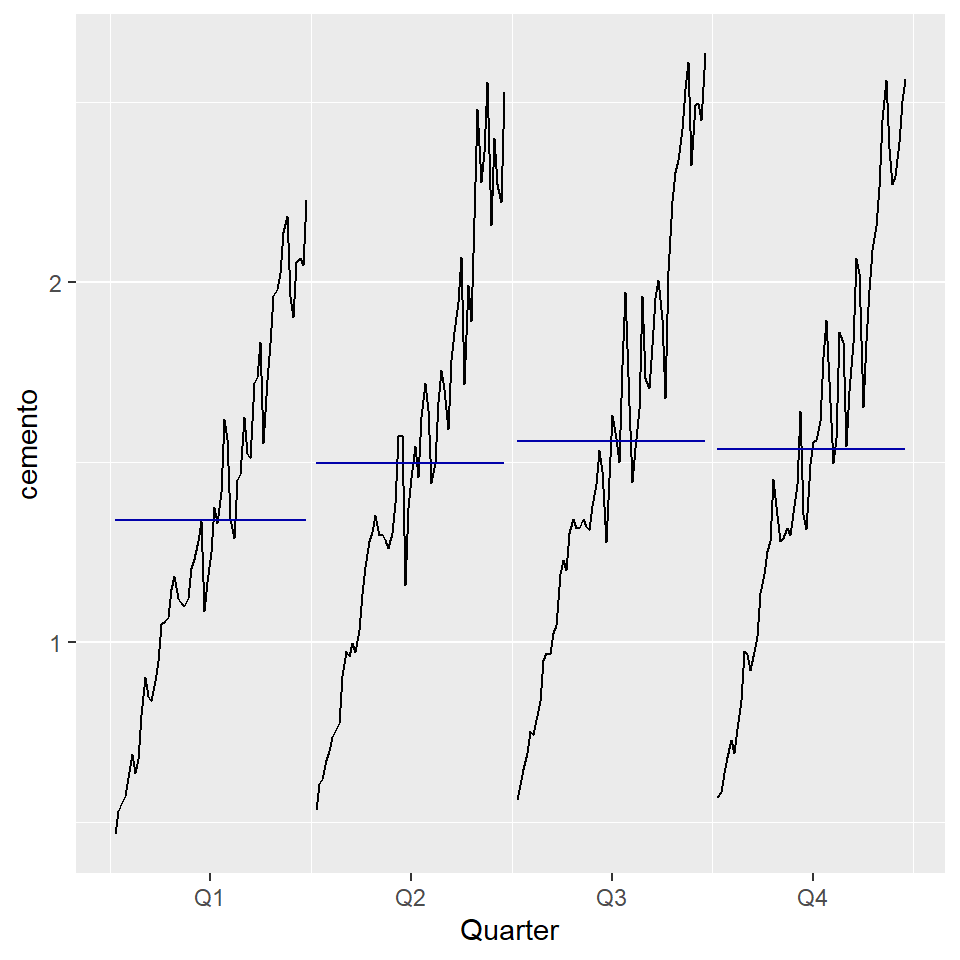

3 Ejemplo: Producción de cemento

Producción trimestral total de cemento en Portland en Australia (en millones de toneladas), desde el primer trimestre de 1956 hasta el primer trimestre de 2014.

cemento<-fpp2::qcement

str(cemento) Time-Series [1:233] from 1956 to 2014: 0.465 0.532 0.561 0.57 0.529 0.604 0.603 0.582 0.554 0.62 ...head(cemento) Qtr1 Qtr2 Qtr3 Qtr4

1956 0.465 0.532 0.561 0.570

1957 0.529 0.604 tail(cemento) Qtr1 Qtr2 Qtr3 Qtr4

2012 2.503

2013 2.049 2.528 2.637 2.565

2014 2.229 - Interpretación de estos gráficos.

autoplot(cemento)

ggseasonplot(cemento, year.labels=FALSE, continuous=TRUE)

ggsubseriesplot(cemento)

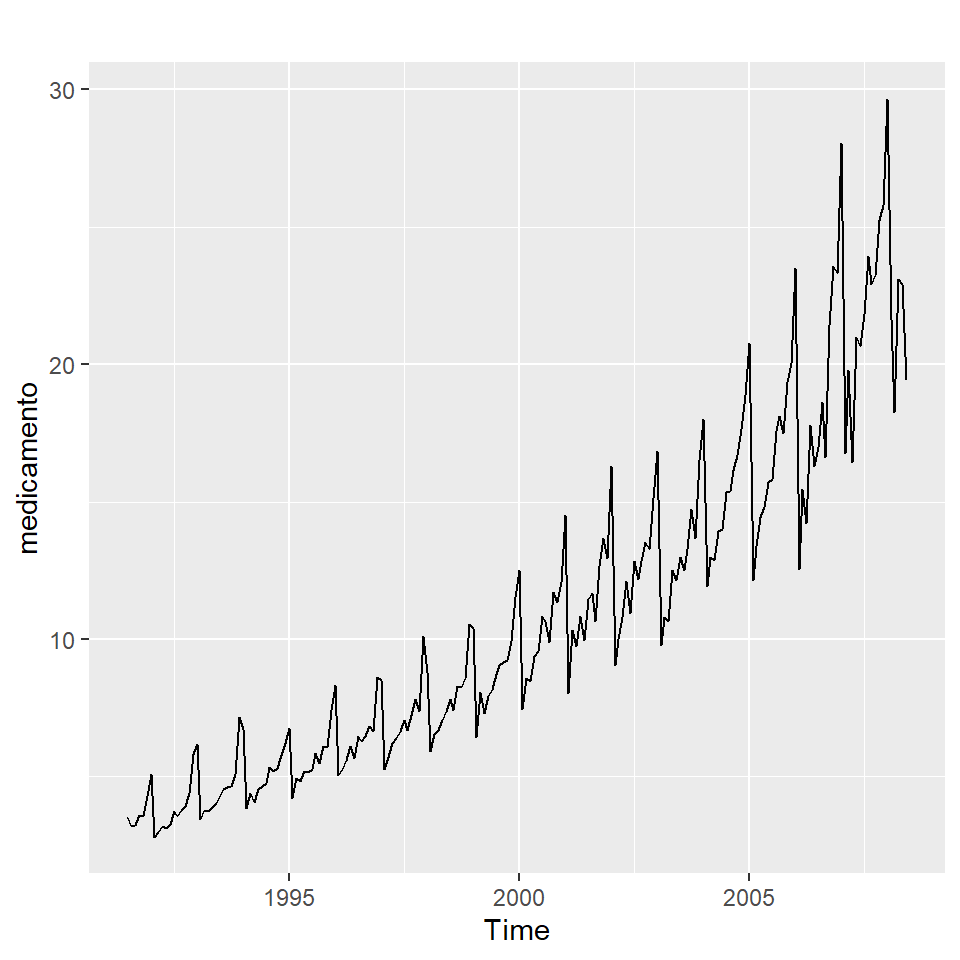

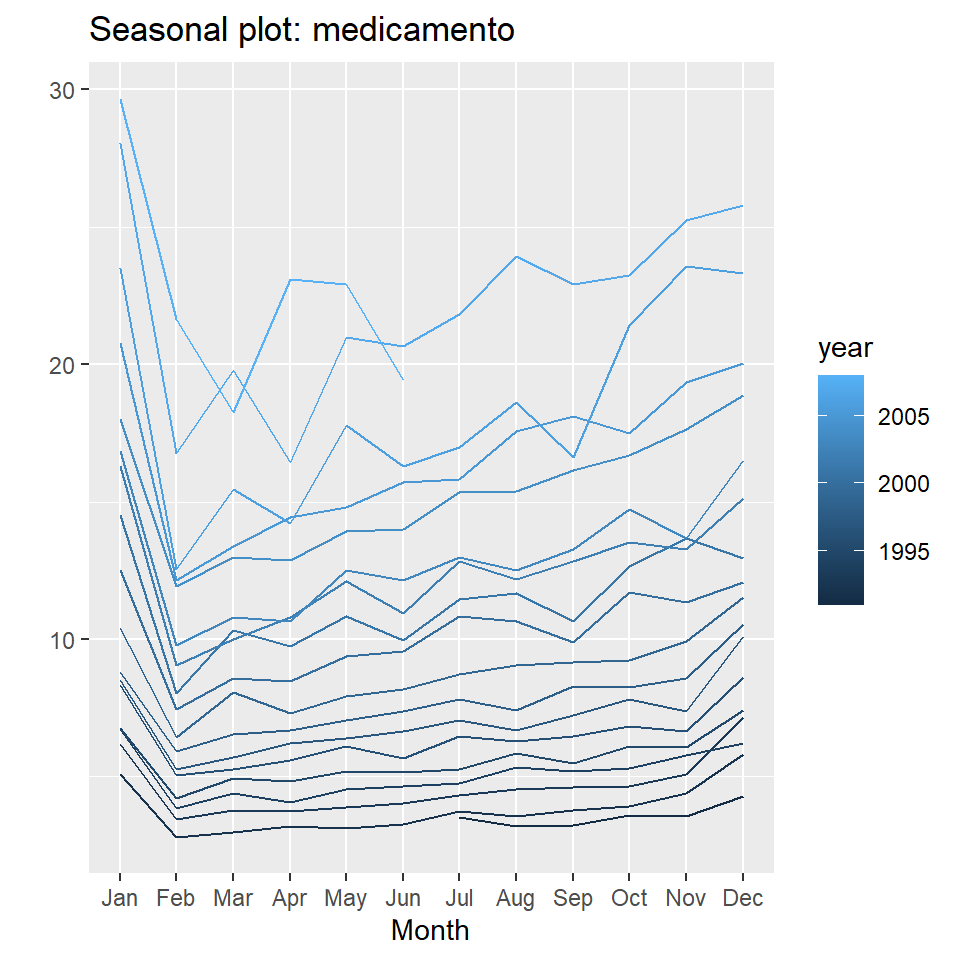

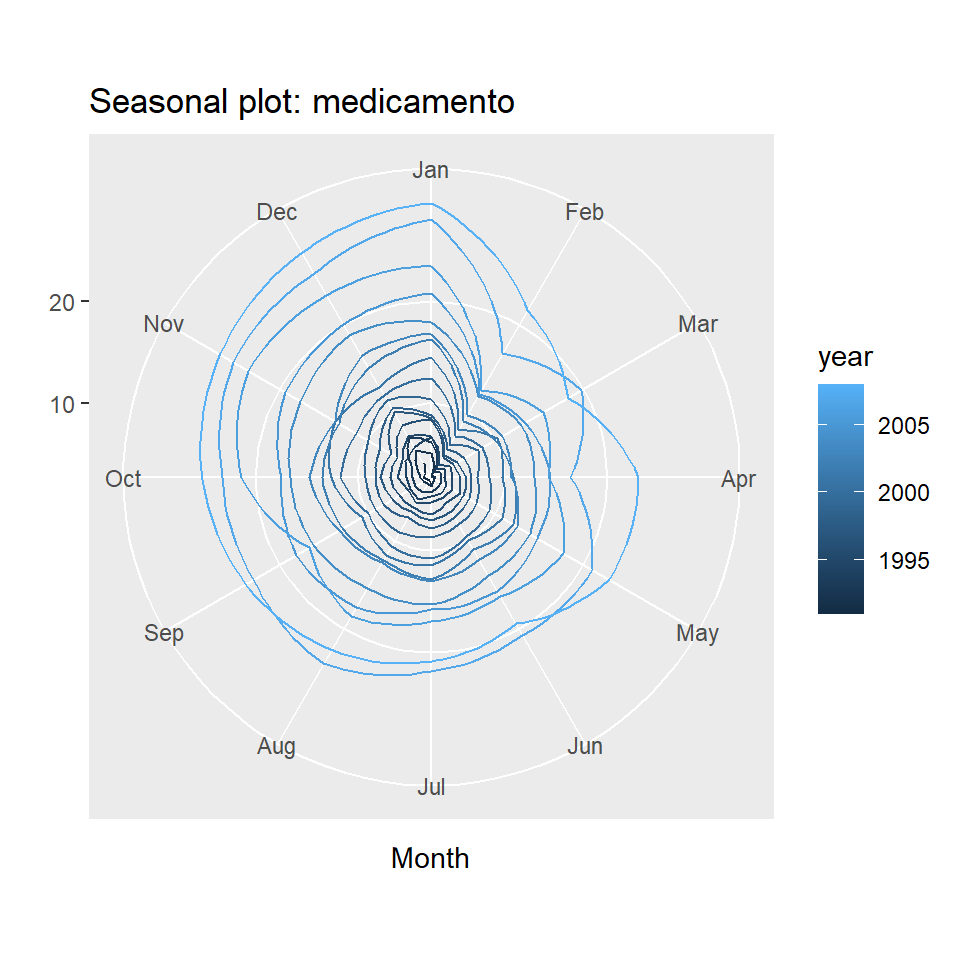

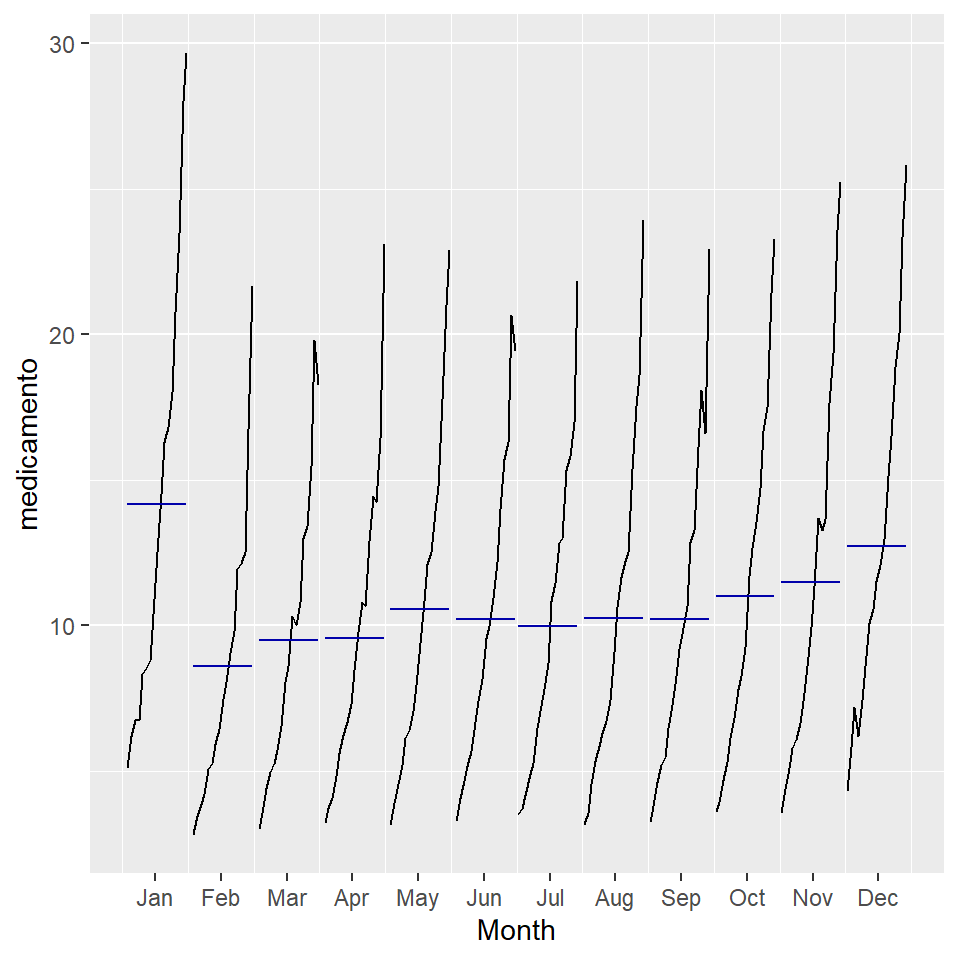

4 Ejemplo: gasto de medicamento anti-diabético (mensual)

Gasto mensual del gobierno (en millones de dólares) de julio de 1991 a junio de 2008.

medicamento<-fpp2::a10- Interpretación de estos gráficos.

autoplot(medicamento)

ggseasonplot(medicamento, year.labels=FALSE, continuous=TRUE)

ggseasonplot(medicamento, year.labels=FALSE, continuous=TRUE, polar = TRUE)

ggsubseriesplot(medicamento)

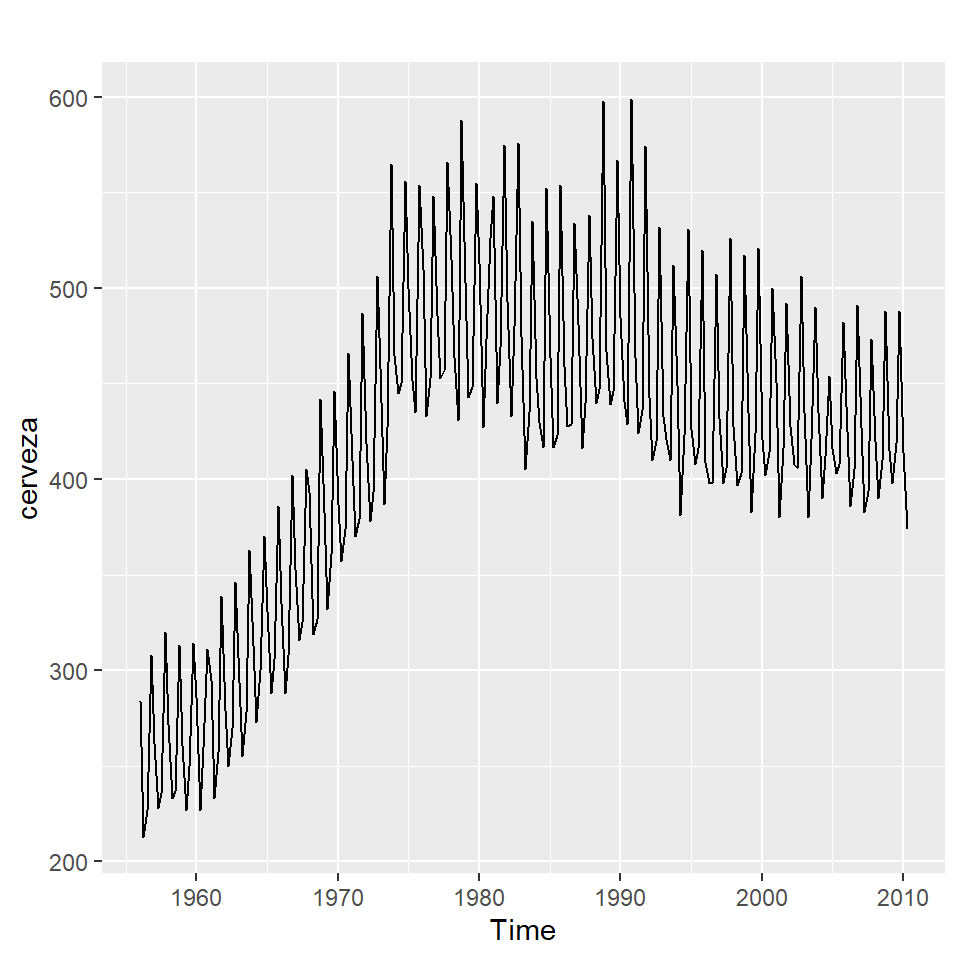

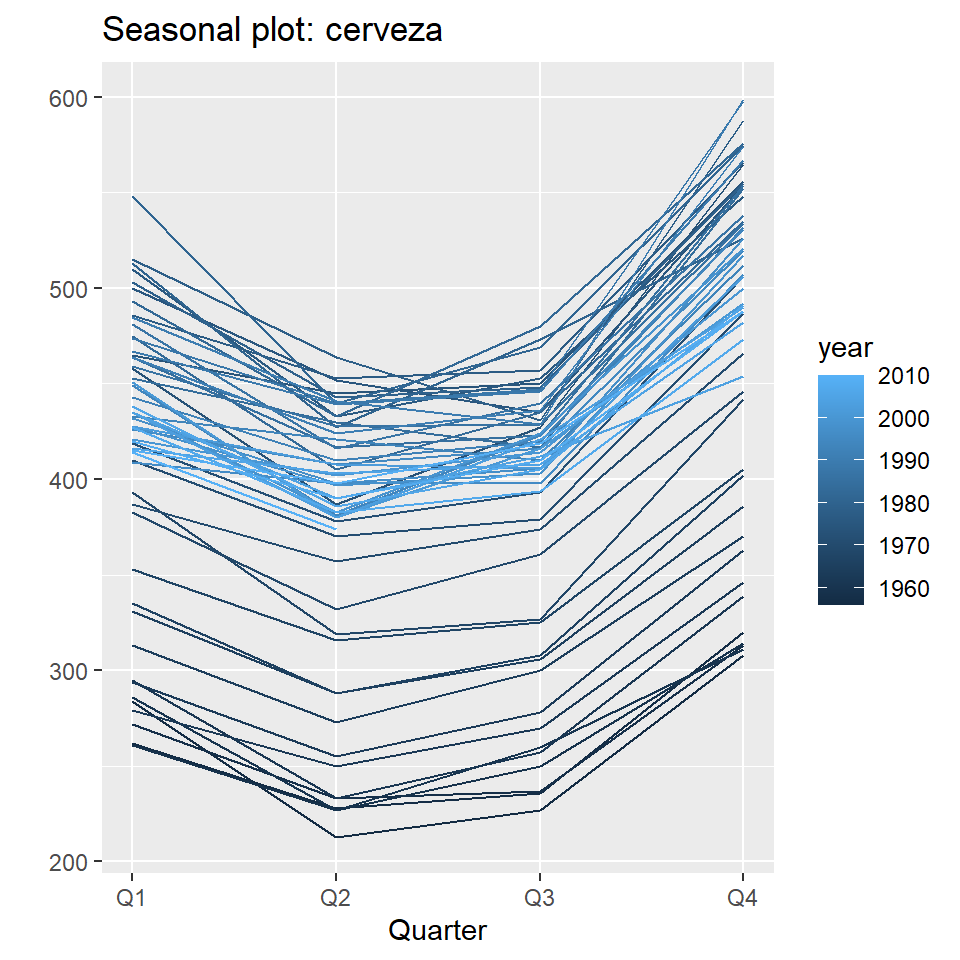

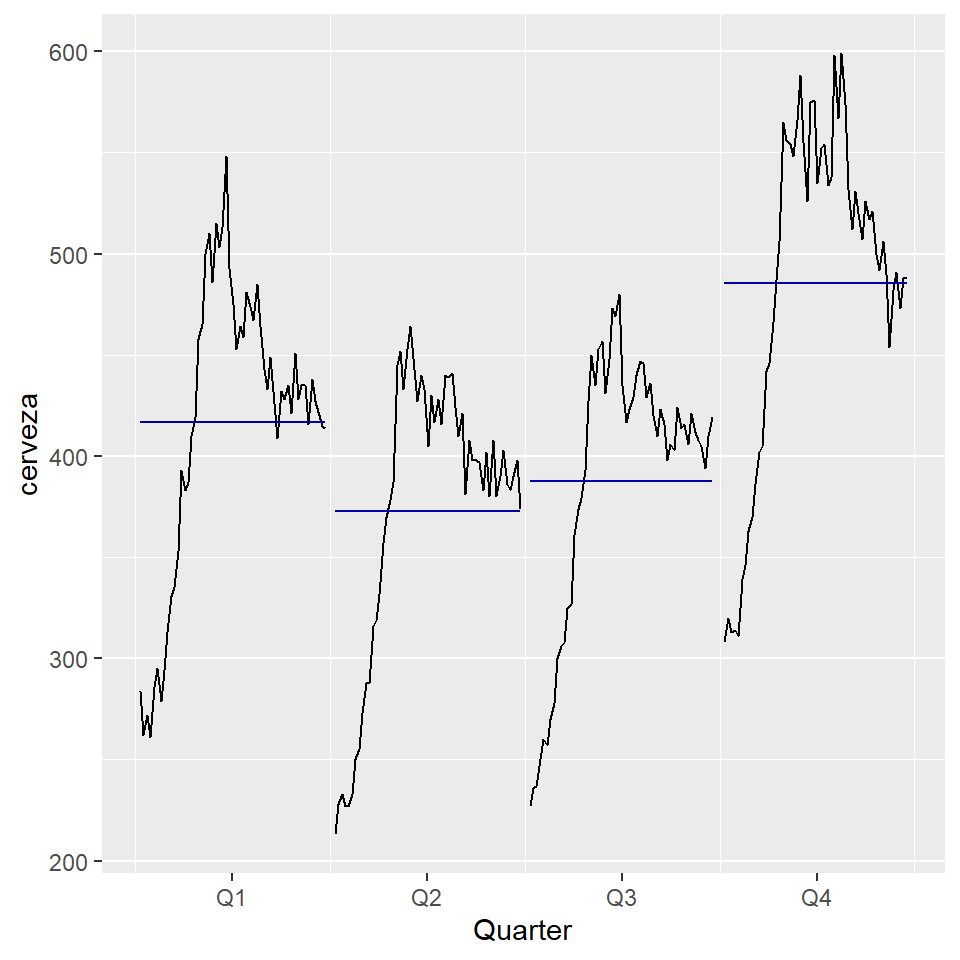

5 Ejemplo: Producción de cerveza en Australia

Producción trimestral total de cerveza en Australia (en megalitros) desde el primer trimestre de 1956 hasta el segundo trimestre de 2010.

cerveza<-fpp2::ausbeer- Interpretación de estos gráficos.

autoplot(cerveza)

ggseasonplot(cerveza, year.labels=FALSE, continuous=TRUE)

ggsubseriesplot(cerveza)

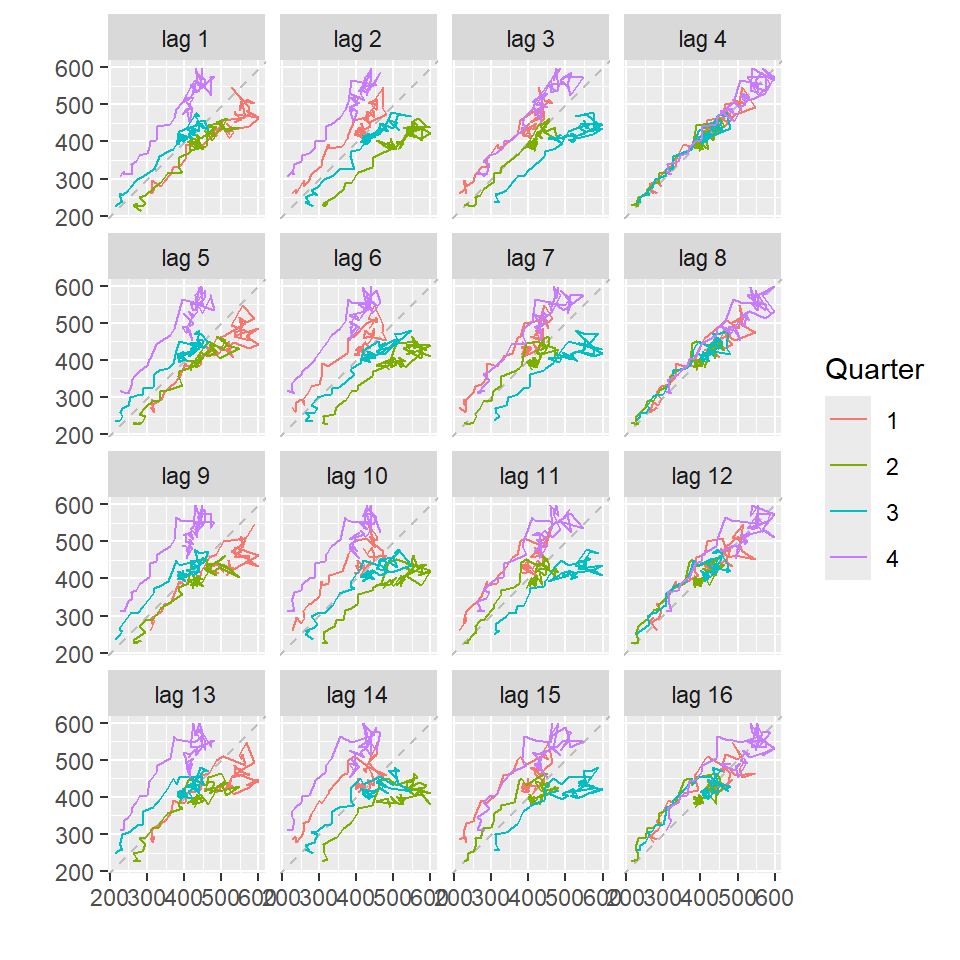

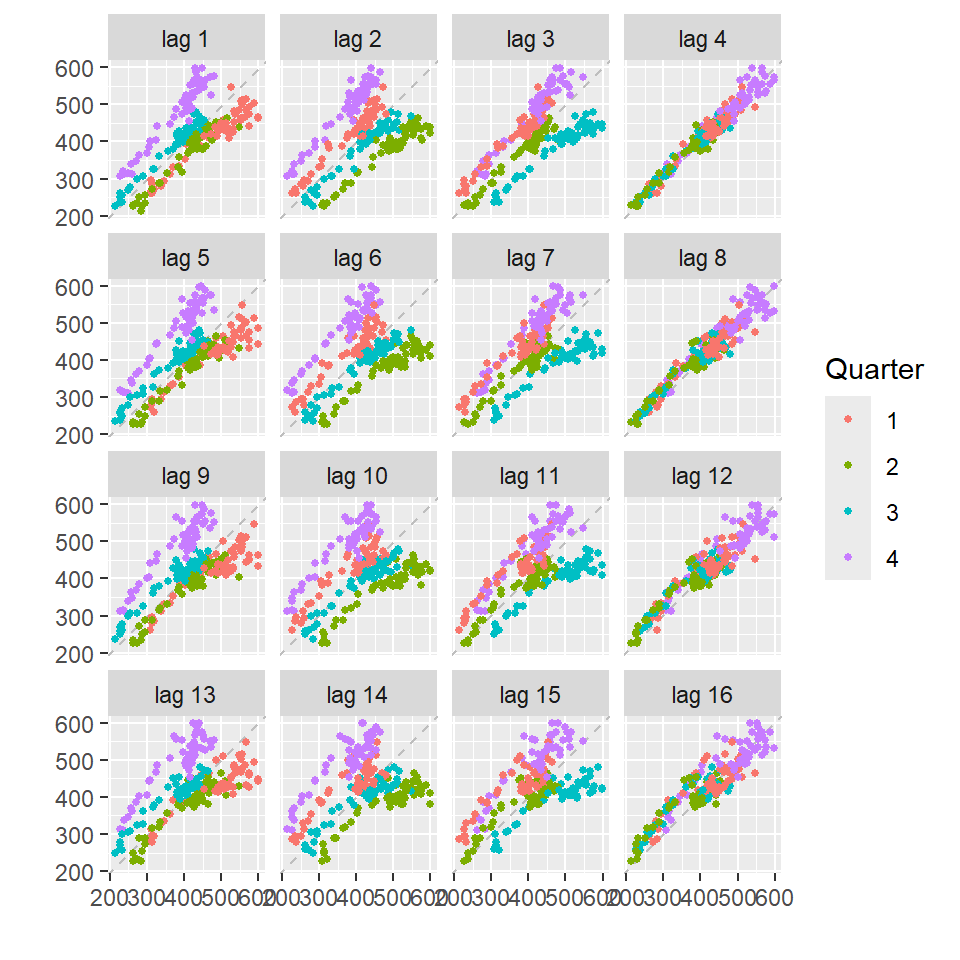

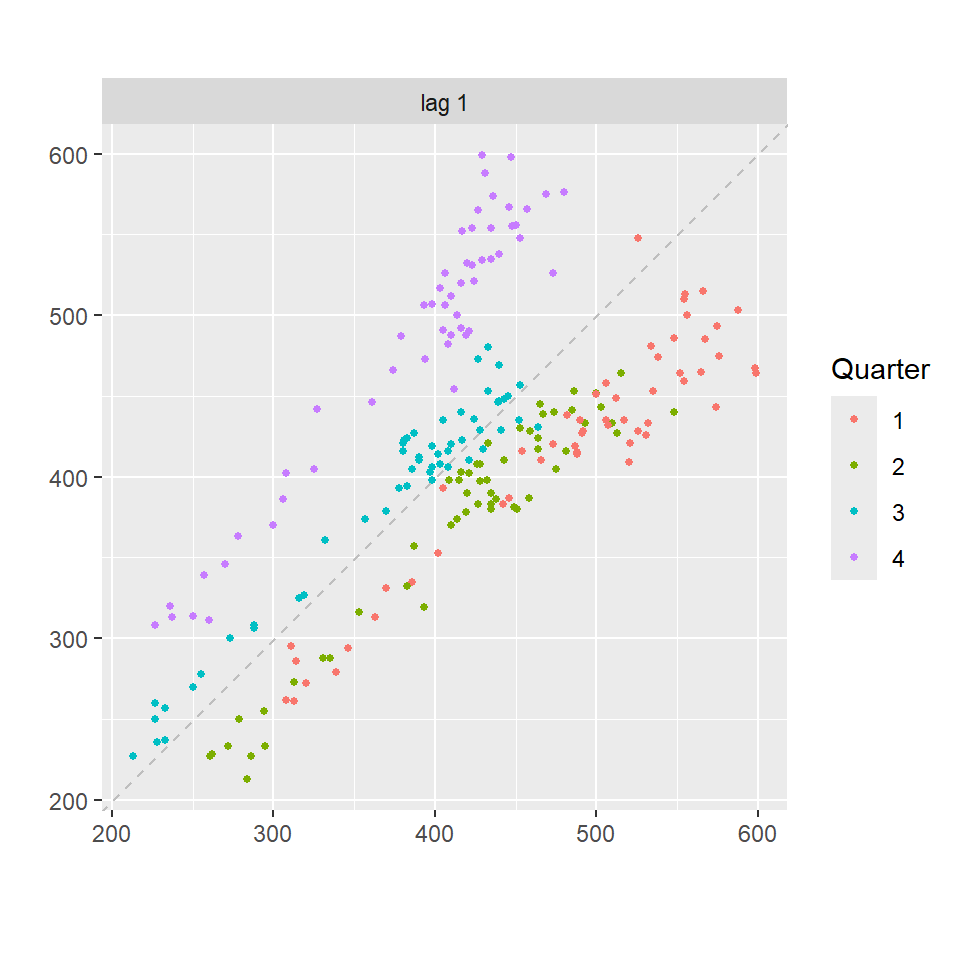

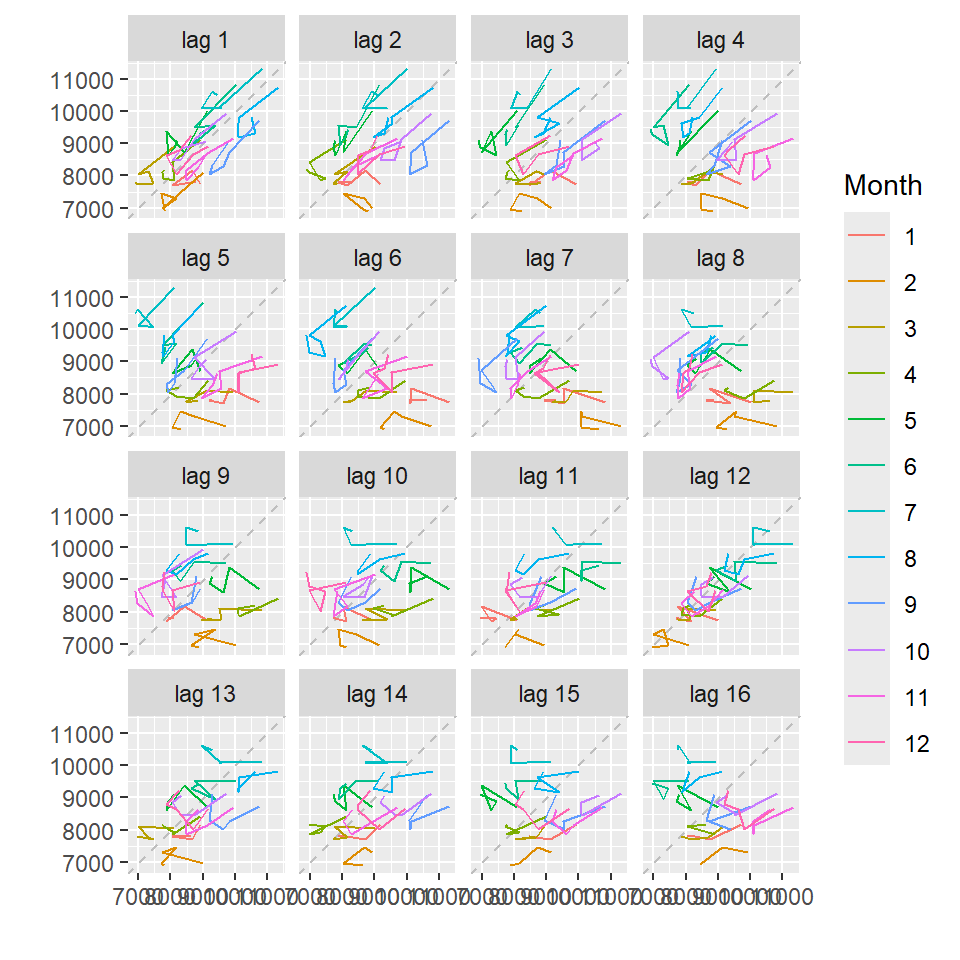

5.1 Gráficos de rezagos

gglagplot(cerveza,lags=16)

gglagplot(cerveza,lags=16,do.lines=FALSE)

h=1

gglagplot(cerveza,lags=h,do.lines=FALSE)

cerveza.shift<-shift(cerveza,n=h,type="lag")

cbind(cerveza,cerveza.shift) cerveza cerveza.shift

1956 Q1 284 NA

1956 Q2 213 284

1956 Q3 227 213

1956 Q4 308 227

1957 Q1 262 308

1957 Q2 228 262

1957 Q3 236 228

1957 Q4 320 236

1958 Q1 272 320

1958 Q2 233 272

1958 Q3 237 233

1958 Q4 313 237

1959 Q1 261 313

1959 Q2 227 261

1959 Q3 250 227

1959 Q4 314 250

1960 Q1 286 314

1960 Q2 227 286

1960 Q3 260 227

1960 Q4 311 260

1961 Q1 295 311

1961 Q2 233 295

1961 Q3 257 233

1961 Q4 339 257

1962 Q1 279 339

1962 Q2 250 279

1962 Q3 270 250

1962 Q4 346 270

1963 Q1 294 346

1963 Q2 255 294

1963 Q3 278 255

1963 Q4 363 278

1964 Q1 313 363

1964 Q2 273 313

1964 Q3 300 273

1964 Q4 370 300

1965 Q1 331 370

1965 Q2 288 331

1965 Q3 306 288

1965 Q4 386 306

1966 Q1 335 386

1966 Q2 288 335

1966 Q3 308 288

1966 Q4 402 308

1967 Q1 353 402

1967 Q2 316 353

1967 Q3 325 316

1967 Q4 405 325

1968 Q1 393 405

1968 Q2 319 393

1968 Q3 327 319

1968 Q4 442 327

1969 Q1 383 442

1969 Q2 332 383

1969 Q3 361 332

1969 Q4 446 361

1970 Q1 387 446

1970 Q2 357 387

1970 Q3 374 357

1970 Q4 466 374

1971 Q1 410 466

1971 Q2 370 410

1971 Q3 379 370

1971 Q4 487 379

1972 Q1 419 487

1972 Q2 378 419

1972 Q3 393 378

1972 Q4 506 393

1973 Q1 458 506

1973 Q2 387 458

1973 Q3 427 387

1973 Q4 565 427

1974 Q1 465 565

1974 Q2 445 465

1974 Q3 450 445

1974 Q4 556 450

1975 Q1 500 556

1975 Q2 452 500

1975 Q3 435 452

1975 Q4 554 435

1976 Q1 510 554

1976 Q2 433 510

1976 Q3 453 433

1976 Q4 548 453

1977 Q1 486 548

1977 Q2 453 486

1977 Q3 457 453

1977 Q4 566 457

1978 Q1 515 566

1978 Q2 464 515

1978 Q3 431 464

1978 Q4 588 431

1979 Q1 503 588

1979 Q2 443 503

1979 Q3 448 443

1979 Q4 555 448

1980 Q1 513 555

1980 Q2 427 513

1980 Q3 473 427

1980 Q4 526 473

1981 Q1 548 526

1981 Q2 440 548

1981 Q3 469 440

1981 Q4 575 469

1982 Q1 493 575

1982 Q2 433 493

1982 Q3 480 433

1982 Q4 576 480

1983 Q1 475 576

1983 Q2 405 475

1983 Q3 435 405

1983 Q4 535 435

1984 Q1 453 535

1984 Q2 430 453

1984 Q3 417 430

1984 Q4 552 417

1985 Q1 464 552

1985 Q2 417 464

1985 Q3 423 417

1985 Q4 554 423

1986 Q1 459 554

1986 Q2 428 459

1986 Q3 429 428

1986 Q4 534 429

1987 Q1 481 534

1987 Q2 416 481

1987 Q3 440 416

1987 Q4 538 440

1988 Q1 474 538

1988 Q2 440 474

1988 Q3 447 440

1988 Q4 598 447

1989 Q1 467 598

1989 Q2 439 467

1989 Q3 446 439

1989 Q4 567 446

1990 Q1 485 567

1990 Q2 441 485

1990 Q3 429 441

1990 Q4 599 429

1991 Q1 464 599

1991 Q2 424 464

1991 Q3 436 424

1991 Q4 574 436

1992 Q1 443 574

1992 Q2 410 443

1992 Q3 420 410

1992 Q4 532 420

1993 Q1 433 532

1993 Q2 421 433

1993 Q3 410 421

1993 Q4 512 410

1994 Q1 449 512

1994 Q2 381 449

1994 Q3 423 381

1994 Q4 531 423

1995 Q1 426 531

1995 Q2 408 426

1995 Q3 416 408

1995 Q4 520 416

1996 Q1 409 520

1996 Q2 398 409

1996 Q3 398 398

1996 Q4 507 398

1997 Q1 432 507

1997 Q2 398 432

1997 Q3 406 398

1997 Q4 526 406

1998 Q1 428 526

1998 Q2 397 428

1998 Q3 403 397

1998 Q4 517 403

1999 Q1 435 517

1999 Q2 383 435

1999 Q3 424 383

1999 Q4 521 424

2000 Q1 421 521

2000 Q2 402 421

2000 Q3 414 402

2000 Q4 500 414

2001 Q1 451 500

2001 Q2 380 451

2001 Q3 416 380

2001 Q4 492 416

2002 Q1 428 492

2002 Q2 408 428

2002 Q3 406 408

2002 Q4 506 406

2003 Q1 435 506

2003 Q2 380 435

2003 Q3 421 380

2003 Q4 490 421

2004 Q1 435 490

2004 Q2 390 435

2004 Q3 412 390

2004 Q4 454 412

2005 Q1 416 454

2005 Q2 403 416

2005 Q3 408 403

2005 Q4 482 408

2006 Q1 438 482

2006 Q2 386 438

2006 Q3 405 386

2006 Q4 491 405

2007 Q1 427 491

2007 Q2 383 427

2007 Q3 394 383

2007 Q4 473 394

2008 Q1 420 473

2008 Q2 390 420

2008 Q3 410 390

2008 Q4 488 410

2009 Q1 415 488

2009 Q2 398 415

2009 Q3 419 398

2009 Q4 488 419

2010 Q1 414 488

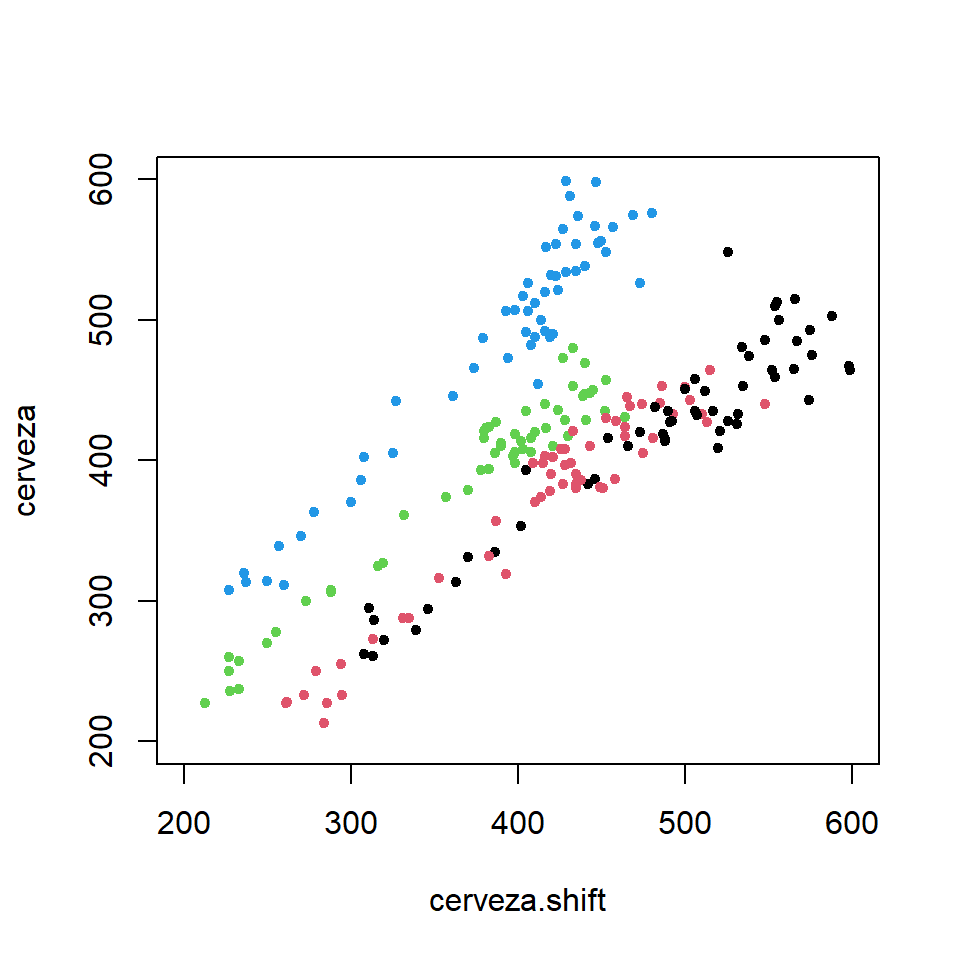

2010 Q2 374 414plot(cerveza~cerveza.shift,xlim=c(200,600),ylim=c(200,600),

xy.labels=FALSE,col=cycle(cerveza),pch=20)

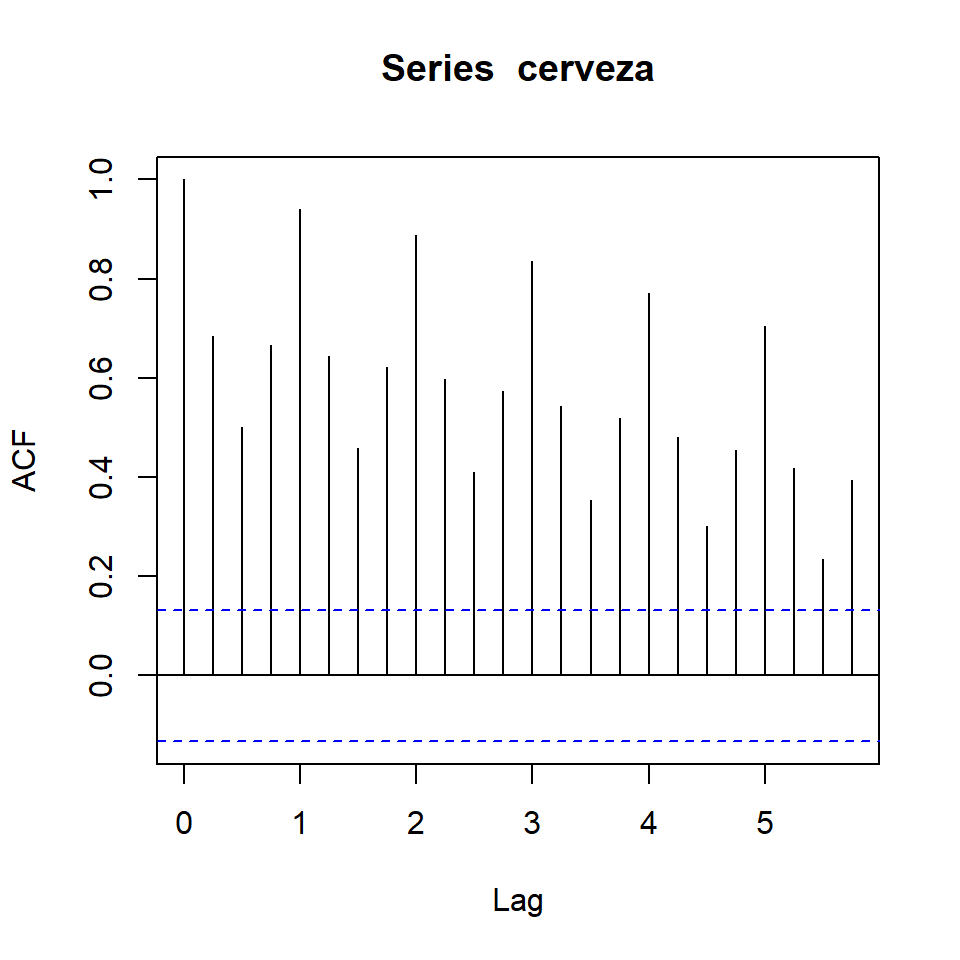

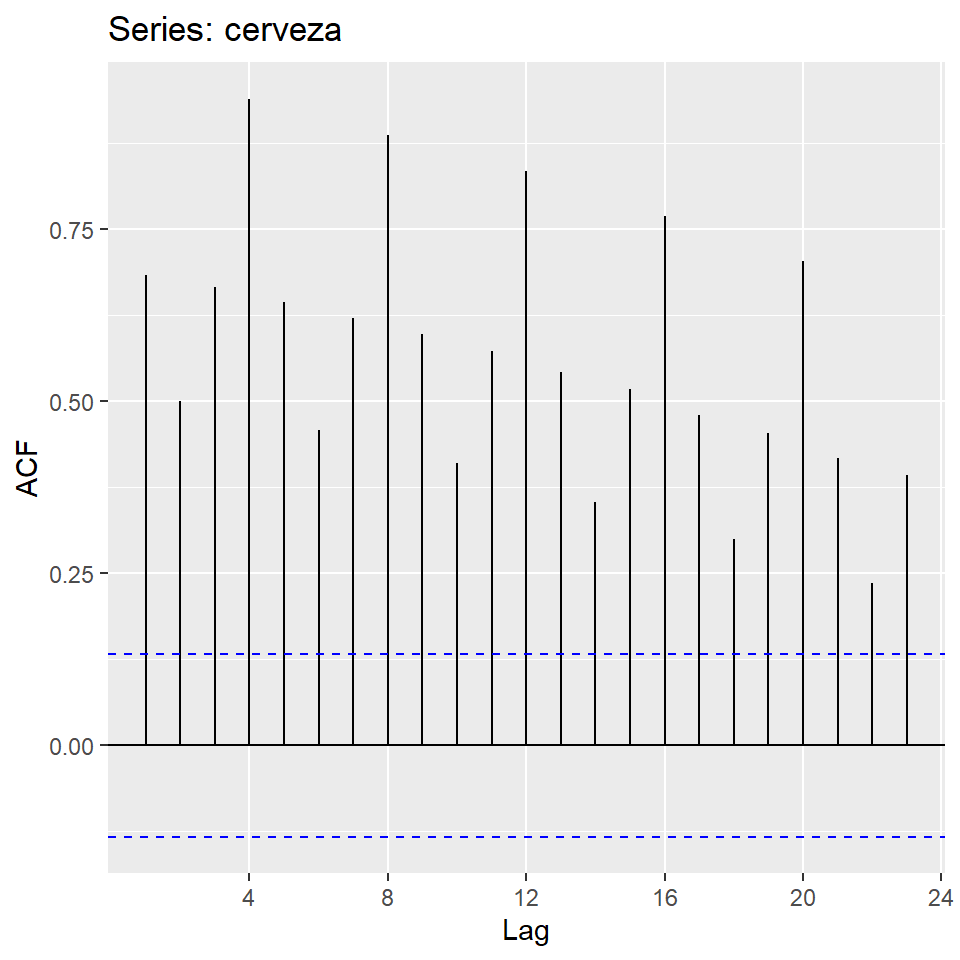

cor(cerveza[-1],cerveza.shift[-1])[1] 0.6876975.2 Funcion de autocorrelacion

acf(cerveza)

ggAcf(cerveza)

acf(ausbeer, plot = FALSE)

Autocorrelations of series 'ausbeer', by lag

0.00 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00 2.25 2.50 2.75 3.00

1.000 0.684 0.500 0.667 0.940 0.644 0.458 0.621 0.887 0.598 0.410 0.574 0.835

3.25 3.50 3.75 4.00 4.25 4.50 4.75 5.00 5.25 5.50 5.75

0.543 0.354 0.519 0.770 0.481 0.300 0.454 0.704 0.418 0.236 0.393 6 Ejemplo: Muertes por accidente en EU 1973-1978

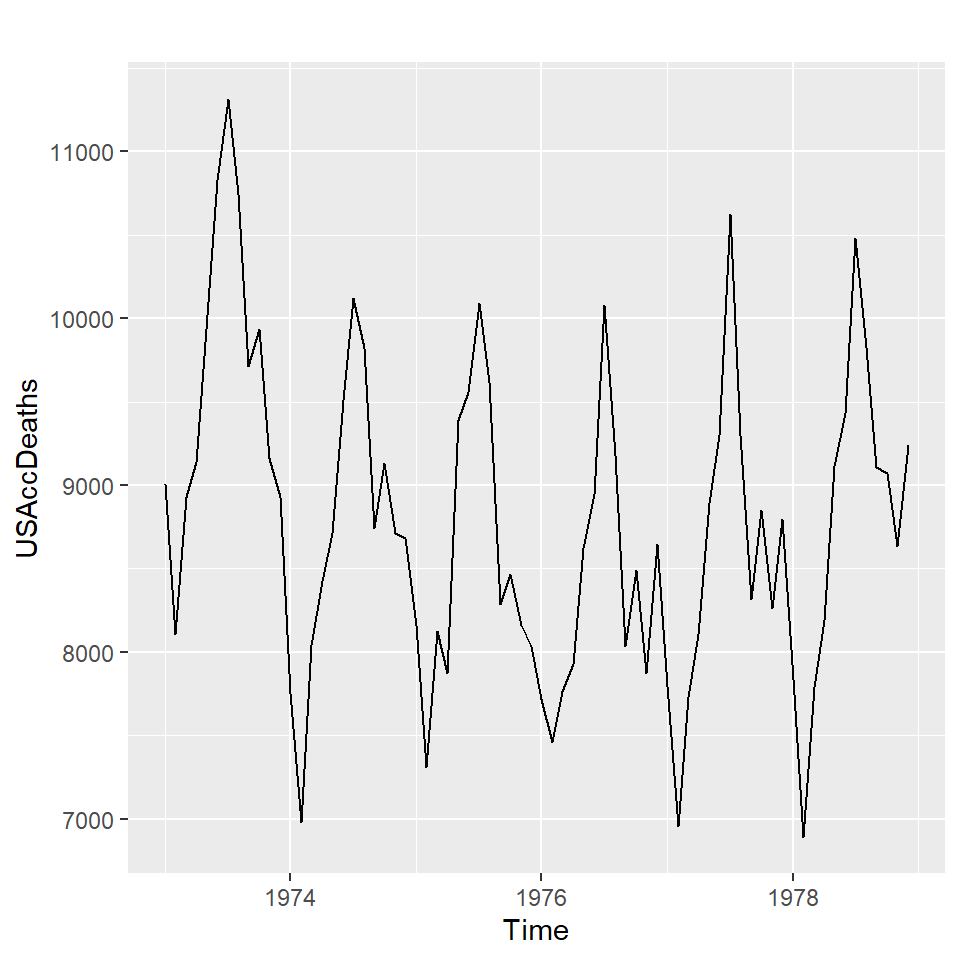

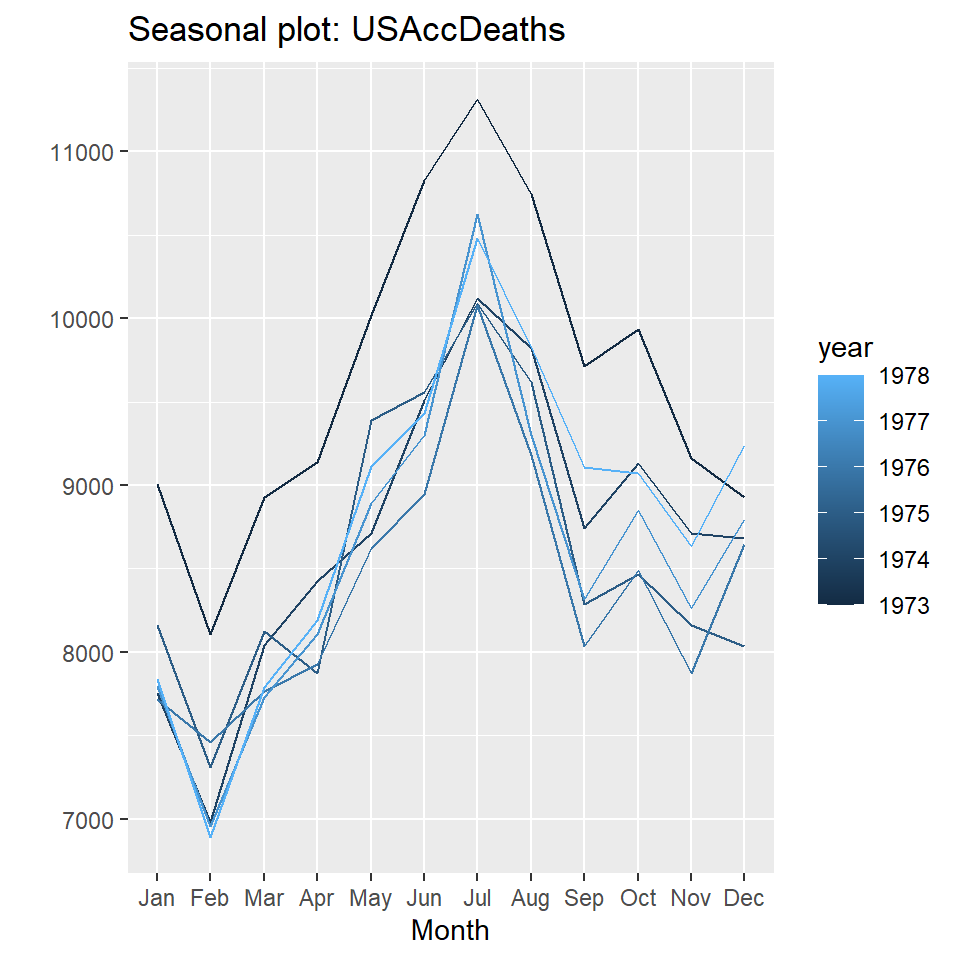

- Interpretación de estos gráficos.

autoplot(USAccDeaths)

ggseasonplot(USAccDeaths, year.labels=FALSE, continuous=TRUE)

gglagplot(USAccDeaths,lags=16)

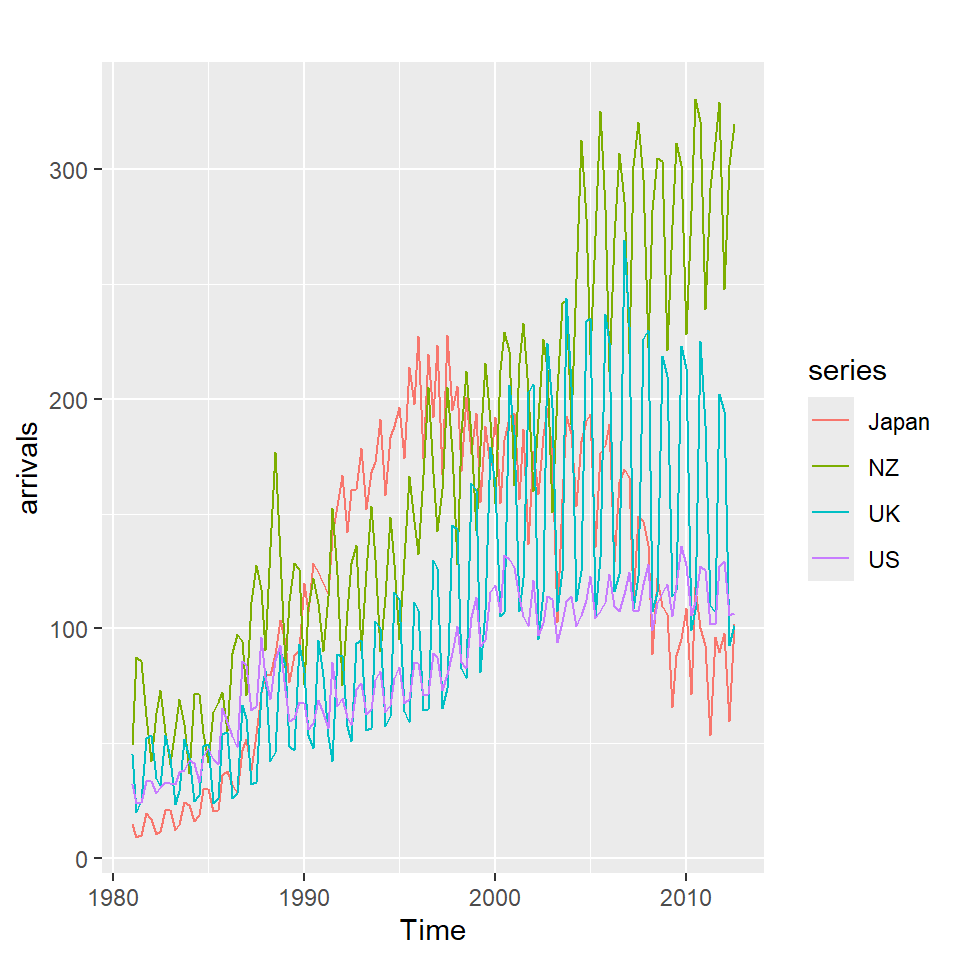

7 Ejemplo: Series multivariadas

arrivals<-fpp2::arrivals

str(arrivals) Time-Series [1:127, 1:4] from 1981 to 2012: 14.76 9.32 10.17 19.51 17.12 ...

- attr(*, "dimnames")=List of 2

..$ : NULL

..$ : chr [1:4] "Japan" "NZ" "UK" "US"arrivals Japan NZ UK US

1981 Q1 14.763 49.140 45.266 32.316

1981 Q2 9.321 87.467 19.886 23.721

1981 Q3 10.166 85.841 24.839 24.533

1981 Q4 19.509 61.882 52.264 33.438

1982 Q1 17.117 42.045 53.636 33.527

1982 Q2 10.617 63.081 34.802 28.366

1982 Q3 11.737 73.275 31.126 30.856

1982 Q4 20.961 54.808 53.619 33.293

1983 Q1 20.671 41.030 43.423 32.472

1983 Q2 12.235 56.155 23.421 32.369

1983 Q3 14.567 69.395 29.142 37.476

1983 Q4 24.363 58.423 51.771 38.112

1984 Q1 23.169 37.039 44.182 42.553

1984 Q2 16.296 71.564 24.920 41.277

1984 Q3 18.504 71.260 27.566 33.056

1984 Q4 29.938 54.597 48.880 44.472

1985 Q1 30.240 41.646 49.563 47.792

1985 Q2 20.280 63.668 23.867 43.070

1985 Q3 20.908 67.803 25.895 41.116

1985 Q4 36.169 72.177 54.092 65.428

1986 Q1 37.989 55.192 54.903 59.377

1986 Q2 32.366 89.073 26.089 53.283

1986 Q3 28.131 97.746 28.248 48.510

1986 Q4 47.150 94.696 66.813 85.878

1987 Q1 51.736 71.130 61.167 84.130

1987 Q2 38.254 111.416 32.400 64.347

1987 Q3 53.807 127.619 33.287 65.976

1987 Q4 71.807 117.078 72.115 96.165

1988 Q1 80.300 90.498 81.925 78.609

1988 Q2 79.596 135.435 42.091 69.306

1988 Q3 88.708 176.899 46.253 86.267

1988 Q4 103.738 131.457 90.062 92.738

1989 Q1 94.172 83.029 84.191 73.321

1989 Q2 76.462 111.748 48.709 59.819

1989 Q3 88.393 128.510 46.905 60.868

1989 Q4 90.527 126.021 93.075 67.761

1990 Q1 119.654 75.584 81.185 67.637

1990 Q2 106.965 109.472 53.693 56.153

1990 Q3 128.472 122.164 48.037 58.783

1990 Q4 124.773 111.222 94.827 69.018

1991 Q1 119.638 90.067 79.365 63.235

1991 Q2 115.049 114.050 52.961 56.691

1991 Q3 140.470 152.662 42.366 85.473

1991 Q4 153.436 123.821 89.041 66.332

1992 Q1 166.732 75.376 87.850 69.861

1992 Q2 141.886 107.369 57.261 61.501

1992 Q3 160.455 128.550 51.058 57.869

1992 Q4 160.807 136.250 93.736 73.632

1993 Q1 178.466 90.758 95.137 76.323

1993 Q2 151.904 124.972 55.661 62.718

1993 Q3 168.131 153.153 56.400 64.731

1993 Q4 172.358 130.393 103.089 77.495

1994 Q1 191.367 90.095 100.250 81.428

1994 Q2 158.207 113.799 57.464 63.554

1994 Q3 183.289 148.605 61.831 66.505

1994 Q4 188.273 127.879 115.736 78.190

1995 Q1 196.480 95.295 112.684 83.047

1995 Q2 174.307 130.073 64.209 67.448

1995 Q3 214.067 166.383 59.287 69.234

1995 Q4 197.850 146.632 111.719 85.160

1996 Q1 227.335 132.410 108.173 84.995

1996 Q2 174.325 166.735 64.632 71.005

1996 Q3 219.347 205.120 64.742 71.412

1996 Q4 192.137 167.569 129.994 89.483

1997 Q1 223.640 142.502 126.261 87.405

1997 Q2 167.269 160.522 65.146 73.061

1997 Q3 227.641 205.250 74.071 79.986

1997 Q4 195.350 177.366 145.139 89.141

1998 Q1 205.468 128.179 143.115 101.167

1998 Q2 168.520 184.943 82.747 85.384

1998 Q3 200.860 212.263 78.303 82.586

1998 Q4 176.235 183.996 163.356 104.760

1999 Q1 193.822 143.015 160.239 113.860

1999 Q2 154.860 179.577 81.152 92.494

1999 Q3 188.080 215.732 107.941 95.001

1999 Q4 170.689 190.461 179.102 115.704

2000 Q1 192.023 154.537 161.953 118.840

2000 Q2 154.701 212.401 105.394 107.313

2000 Q3 182.130 229.048 107.231 131.833

2000 Q4 192.135 221.071 205.874 130.100

2001 Q1 193.645 162.480 184.901 126.702

2001 Q2 156.303 215.840 107.454 113.471

2001 Q3 186.861 233.074 121.889 105.239

2001 Q4 136.748 203.493 202.988 101.058

2002 Q1 177.263 159.879 206.655 121.127

2002 Q2 158.357 191.215 95.564 97.016

2002 Q3 183.821 226.008 115.950 102.261

2002 Q4 196.006 213.000 224.496 114.103

2003 Q1 176.132 150.700 196.276 112.908

2003 Q2 102.633 203.400 107.563 94.212

2003 Q3 156.396 241.800 125.171 102.961

2003 Q4 192.591 243.200 243.894 112.039

2004 Q1 185.175 188.873 205.423 114.017

2004 Q2 153.363 252.262 111.924 101.065

2004 Q3 181.659 312.956 125.132 105.884

2004 Q4 190.143 278.709 233.761 112.335

2005 Q1 193.547 219.527 235.242 122.725

2005 Q2 135.461 270.782 105.370 104.542

2005 Q3 176.242 325.633 131.141 107.725

2005 Q4 180.085 282.908 237.053 111.286

2006 Q1 189.187 212.323 224.933 123.608

2006 Q2 128.920 269.964 116.211 109.865

2006 Q3 163.649 307.149 123.808 107.787

2006 Q4 169.314 286.361 269.292 114.824

2007 Q1 165.823 219.885 231.686 124.677

2007 Q2 111.484 301.654 108.543 108.089

2007 Q3 149.065 320.737 122.734 107.738

2007 Q4 146.673 295.727 226.031 119.189

2008 Q1 136.544 222.770 230.109 128.066

2008 Q2 88.879 282.076 107.430 99.471

2008 Q3 121.951 304.979 115.758 111.243

2008 Q4 109.858 303.481 218.864 115.636

2009 Q1 106.123 221.287 210.109 119.158

2009 Q2 65.748 275.761 113.973 105.507

2009 Q3 88.371 311.431 116.517 118.979

2009 Q4 95.214 301.983 223.178 136.094

2010 Q1 109.072 228.162 213.568 127.535

2010 Q2 71.253 281.791 99.497 105.974

2010 Q3 117.876 330.812 108.208 111.615

2010 Q4 99.987 320.897 225.395 127.002

2011 Q1 92.889 239.103 188.560 125.264

2011 Q2 53.397 292.072 110.212 101.814

2011 Q3 96.467 311.994 107.089 101.925

2011 Q4 89.900 329.470 202.240 127.150

2012 Q1 98.180 247.910 194.640 129.520

2012 Q2 59.760 301.880 92.970 105.700

2012 Q3 101.900 319.840 101.690 106.540autoplot(arrivals)

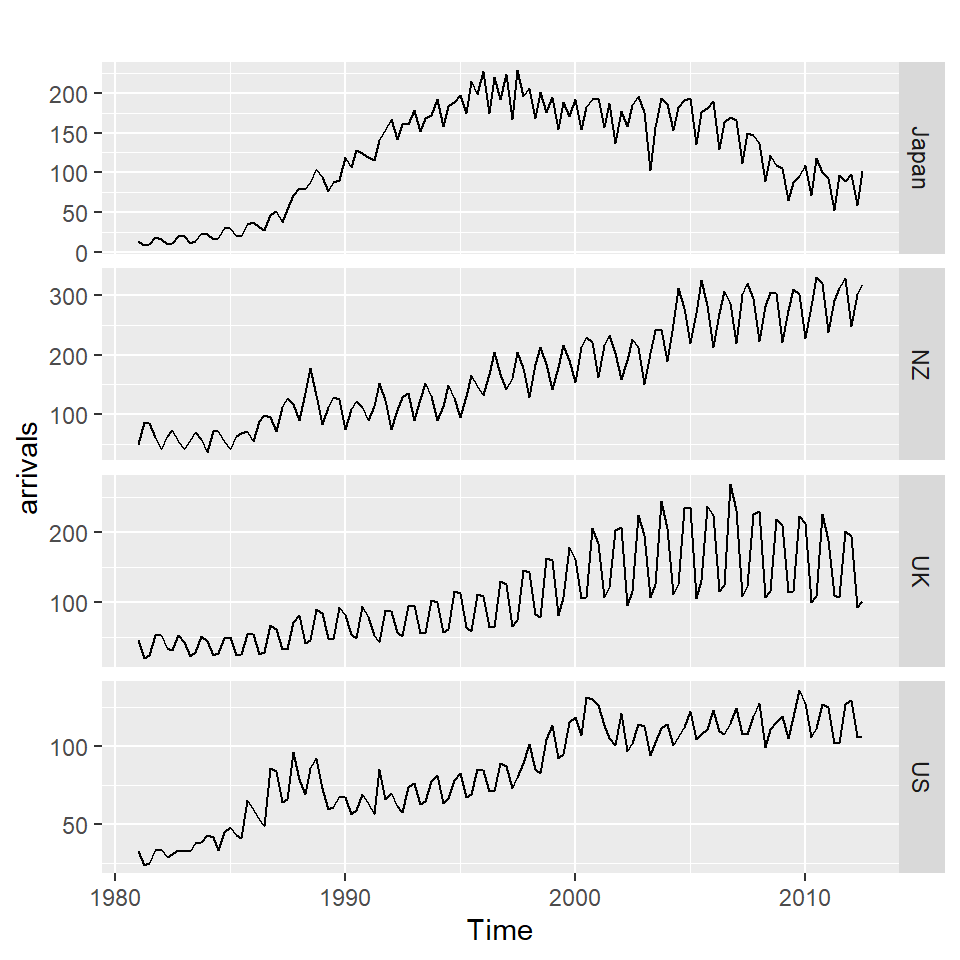

autoplot(arrivals, facets = TRUE)

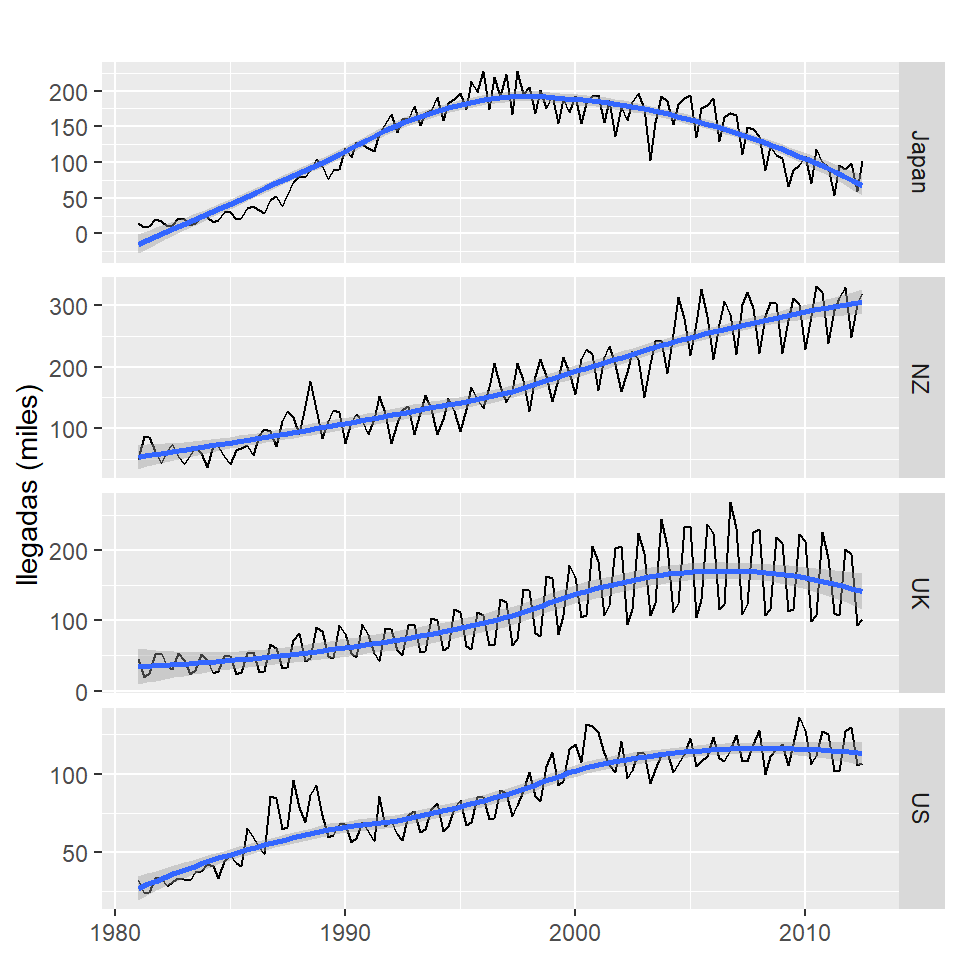

autoplot(arrivals, facets = TRUE) +

geom_smooth() +

labs("Llegadas internacionales a Australia",

y = "llegadas (miles)",

x = NULL)

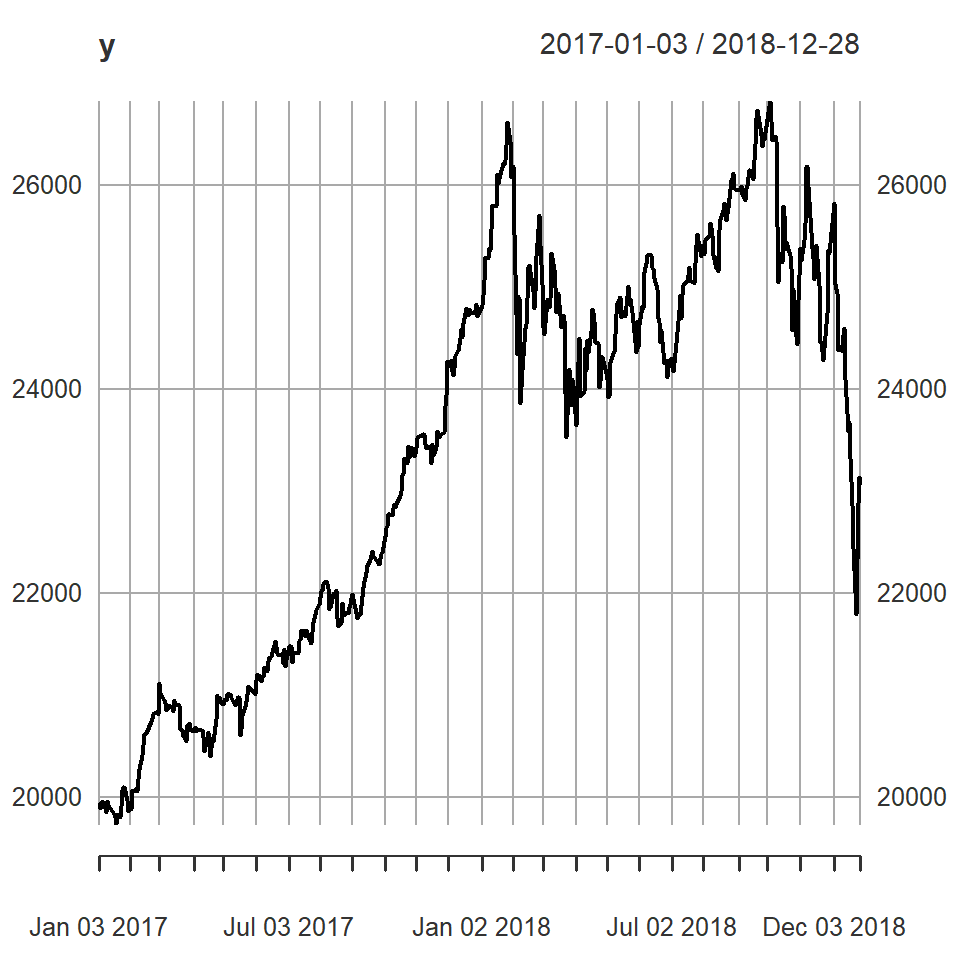

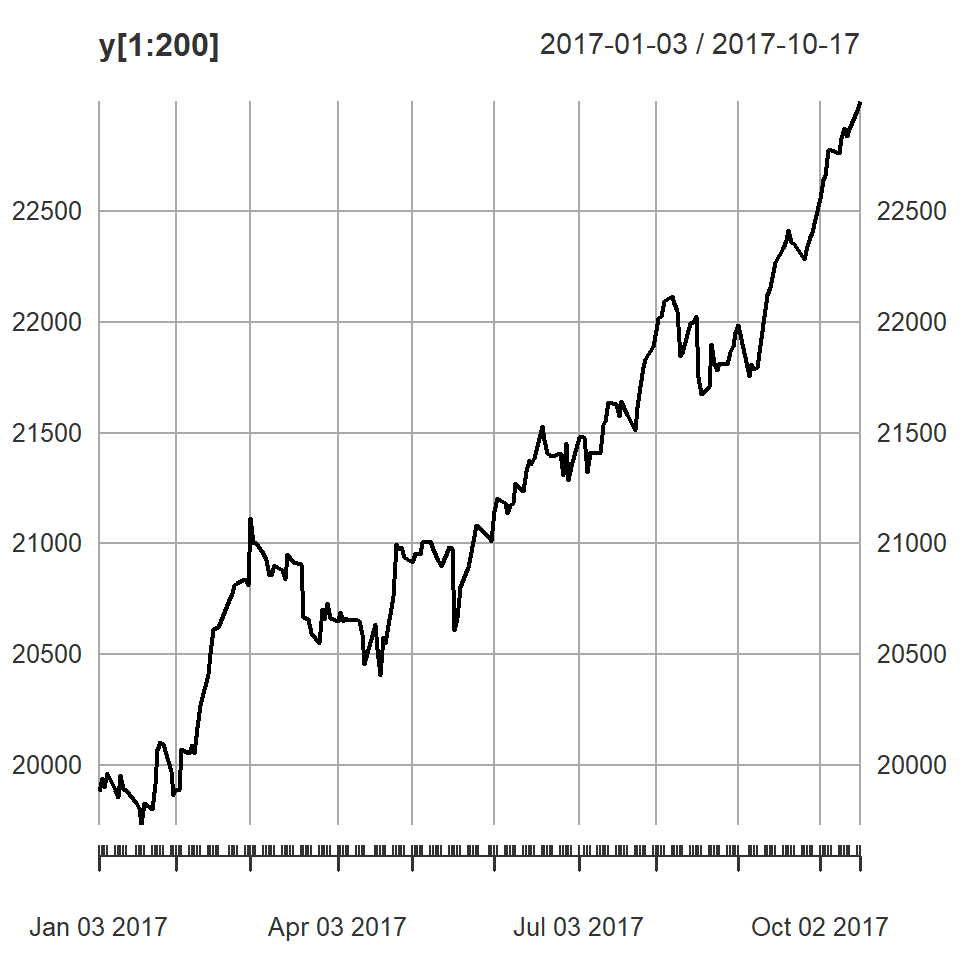

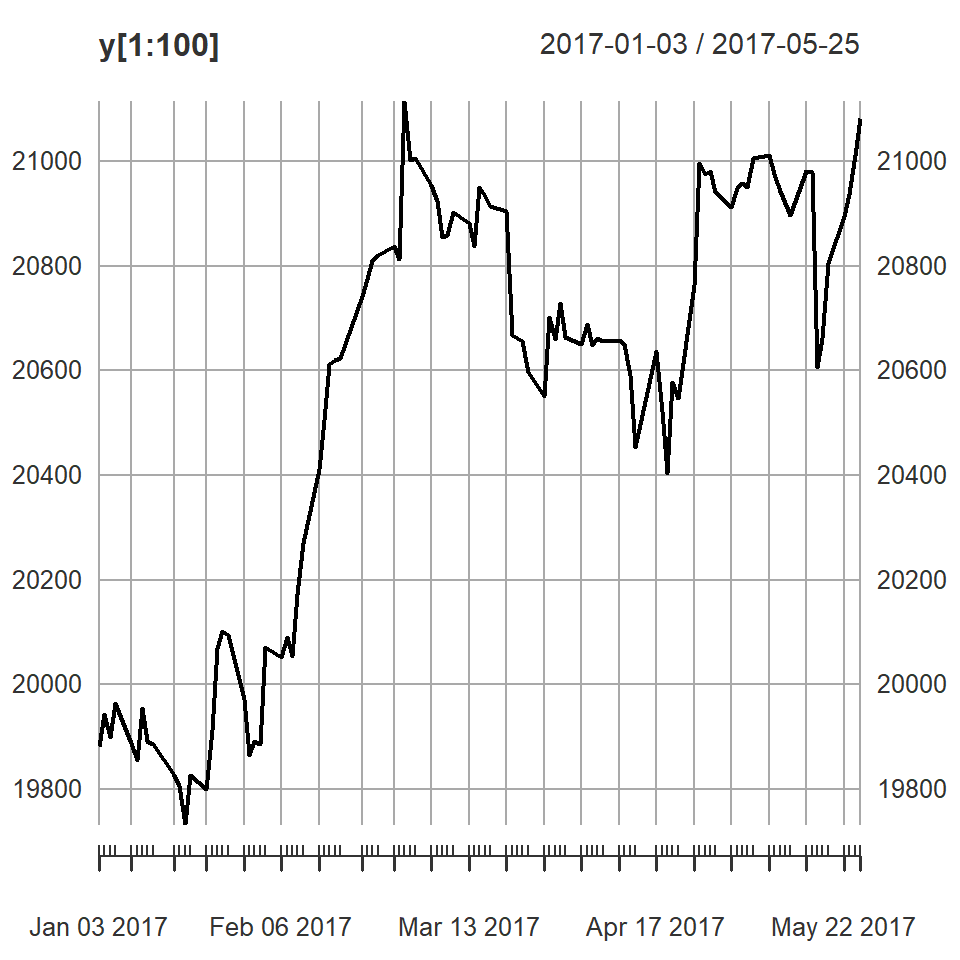

8 Ejemplo: Promedio diario industrial Dow Jone

getSymbols("^DJI",from = "2016/12/31",

to = "2018/12/31",

periodicity = "daily")[1] "DJI"y <- DJI$DJI.Close

library(xts)

plot(y)

#note el comportamiento en diferentes segmentos de tiempo.

plot(y[1:200])

plot(y[1:100])

9 Paquetes en R y extensiones

Existen una variedad de formas de definir objetos de series temporales en R y distintos paquetes para graficar.

https://cran.r-project.org/web/views/TimeSeries.html

Les puede servir: